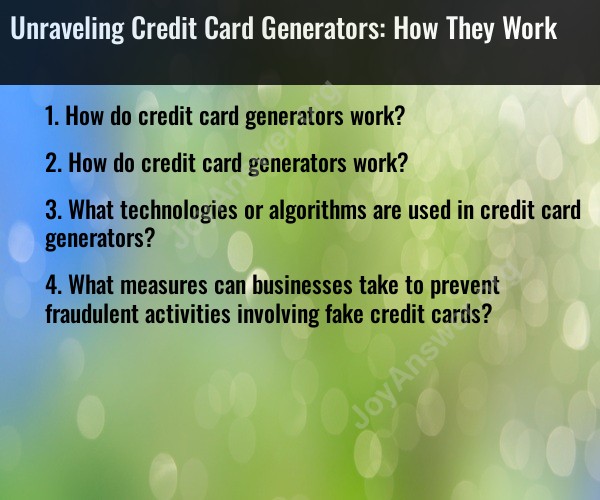

How do credit card generators work?

Credit card generators are tools or software designed to produce fake or valid-looking credit card numbers, often adhering to the format and rules set by payment networks like Visa, Mastercard, or American Express. These generators can have various purposes, ranging from legitimate uses like testing e-commerce platforms to unethical or illegal activities. Here's an explanation of how they work:

1. The Basics of Credit Card Numbering

Credit card numbers are not random; they follow a specific structure and formatting rules:

- Issuer Identification Number (IIN): The first 6 digits identify the card's issuing bank and network (e.g., Visa starts with 4, Mastercard starts with 5).

- Account Number: The next several digits are unique to the cardholder's account.

- Check Digit: The final digit is a checksum calculated using the Luhn algorithm, which ensures the validity of the card number.

2. The Role of the Luhn Algorithm

The Luhn algorithm is a simple checksum formula used to validate credit card numbers. A valid number must satisfy this algorithm:

- Double every second digit from the right.

- If doubling results in a number greater than 9, subtract 9 from it.

- Sum all the digits.

- A valid card number will have a total that ends in 0.

3. How Credit Card Generators Work

Credit card generators produce numbers that conform to these formatting rules:

- Input Parameters: They use predefined Issuer Identification Numbers (IIN) associated with real payment networks and banks.

- Randomized Account Numbers: The account number portion is randomized within valid ranges.

- Checksum Calculation: The generator applies the Luhn algorithm to ensure the final number is valid.

Some generators also produce accompanying details like expiration dates, CVV codes, or names, but these are typically random and do not correspond to real data.

4. Legitimate Uses

- Software Testing: Developers and QA testers use these tools to simulate transactions and test payment gateways without involving real customer data.

- Education and Research: These generators can be used to study how payment systems work without risking privacy or security.

5. Illegitimate Uses

While credit card generators have legitimate applications, they are sometimes misused for fraudulent activities, such as:

- Testing stolen card details.

- Fraudulently bypassing free trials or subscription services.

- Attempting unauthorized transactions.

6. Security and Legal Implications

Using generated credit card numbers for unauthorized purposes is illegal and can lead to severe penalties. Payment systems and financial institutions have robust measures to detect and prevent fraud, such as:

- Requiring additional verification (CVV, 3D Secure, etc.).

- Analyzing transaction patterns for suspicious activity.

- Maintaining blacklists of known fake or compromised numbers.

Conclusion

Credit card generators operate by leveraging the structure and validation rules of real credit card systems, primarily the Luhn algorithm. While they serve valuable roles in testing and education, their misuse for fraudulent activities poses significant risks and legal consequences. Always ensure any use of such tools complies with ethical and legal standards.

How do credit card generators work?

Credit card generators produce numbers that resemble legitimate credit card numbers by following the standard format and validation rules used by payment networks like Visa, Mastercard, and American Express.

Number Structure: Credit card numbers have a specific format:

- Issuer Identification Number (IIN): The first 6 digits identify the card's issuer and network.

- Account Number: The digits following the IIN represent the cardholder’s account.

- Check Digit: The final digit is a checksum calculated using the Luhn algorithm to ensure the number is valid.

Steps in Generation:

- A predefined IIN for a specific card issuer is chosen.

- The account number portion is generated randomly within valid ranges.

- The generator calculates the check digit using the Luhn algorithm to ensure the number passes validation.

Output: The generated number may include additional fake details like expiration dates or CVV codes, but these are not linked to any real accounts.

What technologies or algorithms are used in credit card generators?

Credit card generators rely on specific technologies and algorithms to create valid-looking numbers:

Luhn Algorithm:

- A simple checksum formula used to validate the integrity of a credit card number.

- It ensures the generated number adheres to payment network rules.

Randomization Algorithms:

- These are used to generate the unique account number portion of the credit card.

- They ensure the output doesn’t produce predictable or repetitive results.

Predefined IIN Libraries:

- Generators use databases of valid IINs for various payment networks and card issuers.

- This ensures that the generated number appears legitimate when matched with issuer information.

Additional Details Generation:

- Random generators produce fake expiration dates, CVV codes, and names to simulate complete card details.

- These details are often nonsensical or random and don’t correspond to any real accounts.

What measures can businesses take to prevent fraudulent activities involving fake credit cards?

Businesses can adopt several measures to reduce fraud risks associated with fake credit cards:

a. Implement Advanced Fraud Detection

Address Verification System (AVS):

- Verifies that the billing address provided matches the address on file with the card issuer.

Card Verification Value (CVV) Checks:

- Require the CVV (3 or 4-digit code) for transactions and validate it during processing.

3D Secure Authentication:

- Adds an extra layer of security through a password or biometric verification (e.g., Verified by Visa, Mastercard SecureCode).

b. Monitor Transactions for Suspicious Behavior

- Analyze Patterns:

- Look for unusual transaction patterns like frequent small charges or repeated failed payment attempts.

- Velocity Checks:

- Limit the number of transactions allowed from the same IP address, card, or account in a short time.

c. Validate and Tokenize Payment Data

- Real-Time Validation:

- Use third-party services to validate card details against issuing banks in real time.

- Tokenization:

- Replace sensitive card information with tokens to minimize the risk of storing real card data.

d. Use Machine Learning and AI Tools

- Fraud Detection Systems:

- Implement machine learning tools to identify and flag potentially fraudulent transactions.

- Use AI to adapt to evolving fraud techniques.

e. Regularly Update Security Measures

- Compliance with PCI DSS Standards:

- Ensure compliance with the Payment Card Industry Data Security Standard.

- Update Systems:

- Keep anti-fraud systems, firewalls, and other security software up to date.

f. Educate Customers and Staff

- Awareness Campaigns:

- Teach customers to identify phishing attempts and secure their card details.

- Training Staff:

- Train employees to recognize fraudulent activities and take appropriate action.

By combining these measures, businesses can significantly reduce the risk of fraud stemming from fake credit card numbers.