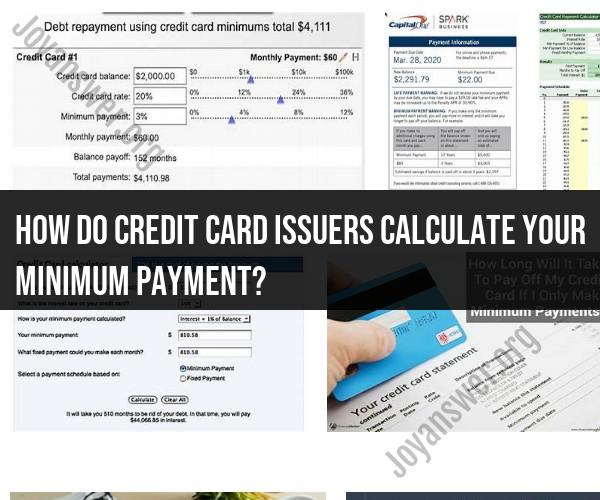

How do credit card issuers calculate your minimum payment?

Credit card issuers use various methods to calculate the minimum payment required for your credit card bill. While specific calculations can vary between issuers, the most common method used is a percentage of your outstanding balance plus any fees and interest charges. Here's a general overview of how credit card issuers calculate minimum payments:

Percentage Method: The most common method is to calculate the minimum payment as a percentage of your outstanding balance. This percentage typically falls in the range of 1% to 3% of the balance. The exact percentage may vary depending on your credit card issuer's terms and conditions.

Interest and Fees: In addition to the percentage of the outstanding balance, the minimum payment may also include any interest charges and fees that have accrued on the account since the last billing cycle. This ensures that you are at least covering the cost of interest and any additional charges.

Floor Amount: Some credit card issuers set a minimum floor amount, which means that the minimum payment cannot be less than a specified dollar amount. For example, even if the calculated percentage-based minimum payment is less than $25, the floor amount may require you to pay at least $25.

Grace Period: Credit card issuers typically provide a grace period, which is the time between the end of the billing cycle and the payment due date. If you pay your statement balance in full during the grace period, you won't incur interest charges on new purchases. However, if you only make the minimum payment or less, you may lose the grace period and start accruing interest on new purchases immediately.

It's important to understand that making only the minimum payment can result in high-interest costs and a longer time to pay off your balance. If you can afford to pay more than the minimum, it's generally advisable to do so to reduce your overall interest expenses and pay down your balance more quickly.

Additionally, credit card issuers are required to disclose how they calculate the minimum payment in your credit card agreement and on your monthly statement. Reviewing this information can help you understand how your minimum payment is determined and make informed decisions about managing your credit card debt.

What Goes into the Calculation of Credit Card Minimum Payments?

Credit card minimum payments are calculated using a formula that takes into account your current balance, interest rate, and any other fees that may apply. The most common formula used to calculate minimum payments is as follows:

Minimum payment = (Statement balance - credits) * (Interest rate + Fees)

The statement balance is the total amount of money you owe on your credit card at the end of your billing cycle. Credits can include things like returns or payments you have made that have not yet been posted to your account.

The interest rate is the percentage of your credit card balance that you are charged each month for carrying a balance. Fees can include things like late payment fees, annual fees, and foreign transaction fees.

How Credit Card Issuers Determine Minimum Payments

Credit card issuers are required by law to set minimum payments that are at least 1% of your statement balance, plus any interest and fees that have accrued. However, most credit card issuers set minimum payments that are higher than this.

The exact formula that credit card issuers use to calculate minimum payments is typically kept confidential. However, it is believed that most issuers use a formula that is based on the following factors:

- Your creditworthiness: Credit card issuers are more likely to set lower minimum payments for borrowers with good credit scores.

- Your payment history: If you have a history of making on-time payments, your credit card issuer is more likely to set a lower minimum payment.

- Your credit utilization: Your credit utilization is the amount of credit you are using compared to your total available credit. If your credit utilization is high, your credit card issuer is more likely to set a higher minimum payment.

How to Master the Minimum

It is important to note that making only the minimum payment on your credit card will not pay off your balance quickly. In fact, if you only make the minimum payment, you will likely end up paying more in interest over time.

If you want to pay off your credit card balance quickly, you should try to make more than the minimum payment each month. You can also try to transfer your balance to a credit card with a lower interest rate.

Here are some tips for mastering the credit card minimum:

- Understand how your minimum payment is calculated.

- Make at least the minimum payment on time each month to avoid late payment fees.

- Try to make more than the minimum payment each month to pay off your balance faster.

- Consider transferring your balance to a credit card with a lower interest rate.

If you are struggling to make your credit card payments, it is important to reach out for help. There are a number of organizations that offer credit counseling and debt consolidation services.