How to calculate mortgage eligibility?

Calculating mortgage eligibility involves assessing various financial factors to determine how much a lender may be willing to lend you for a home purchase. Here are the key steps involved:

Evaluate Your Income: Determine your gross monthly income. Lenders typically use your pre-tax income when calculating eligibility. Include income from all sources, such as employment, investments, rental properties, and any other stable income streams.

Assess Your Debts: Calculate your monthly debt obligations, including credit card payments, car loans, student loans, and any other outstanding debts. Lenders consider your debt-to-income ratio (DTI), which is the percentage of your gross monthly income that goes toward paying debts.

Determine Your Down Payment: Decide how much you can afford to put down as a down payment. Most lenders require a down payment, typically ranging from 3% to 20% of the home's purchase price. A larger down payment can lower your monthly mortgage payments and improve your eligibility.

Estimate Property Taxes and Insurance: Consider the property taxes and homeowners insurance costs associated with the homes you're considering. These expenses are often included in your monthly mortgage payment, so lenders factor them into your eligibility calculations.

Calculate Your Maximum Monthly Mortgage Payment: Lenders typically use a debt-to-income ratio guideline to determine the maximum mortgage payment you can afford. This ratio varies but is often around 28-36% of your gross monthly income. Use this percentage to calculate the maximum monthly mortgage payment you can afford based on your income.

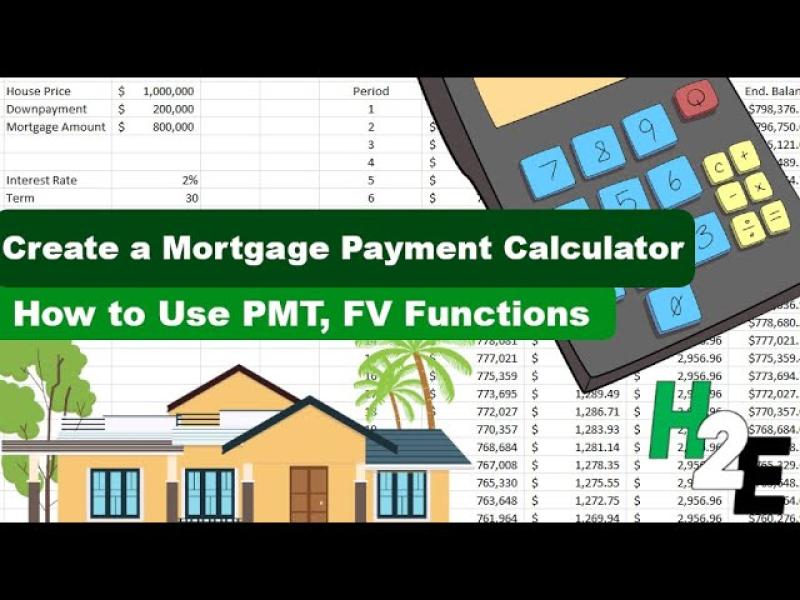

Determine Your Maximum Loan Amount: Based on your maximum monthly mortgage payment and prevailing interest rates, calculate the maximum loan amount you can afford using online mortgage calculators or formulas provided by lenders. This calculation considers factors like the loan term (e.g., 30 years), interest rate, and other terms.

Get Pre-Qualified or Pre-Approved: Once you have a rough estimate of your mortgage eligibility, consider getting pre-qualified or pre-approved for a mortgage from a lender. Pre-qualification provides an estimate based on your self-reported financial information, while pre-approval involves a more comprehensive review of your finances by the lender.

Consider Additional Factors: Keep in mind that lenders may consider other factors when assessing your mortgage eligibility, such as your credit score, employment history, savings, and overall financial stability. Maintaining a strong credit profile and stable financial situation can improve your chances of qualifying for a mortgage and obtaining favorable loan terms.

By following these steps and consulting with a mortgage lender or financial advisor, you can gain a better understanding of your mortgage eligibility and make informed decisions when purchasing a home.

Mortgage Eligibility: Factors, Assessment, and Improvement

Getting a mortgage involves meeting specific criteria set by lenders. Here's a breakdown of what influences your eligibility:

1. Factors influencing mortgage eligibility:

- Credit Score: This is the most significant factor, with higher scores indicating better creditworthiness and lower loan risk.

- Debt-to-Income Ratio (DTI): This measures your monthly debt payments compared to your gross income. Lower DTIs (typically below 36%) suggest better ability to manage additional debt.

- Down Payment: A larger down payment reduces the loan amount needed, lowering risk for the lender and potentially qualifying you for better rates.

- Employment History: Steady employment with sufficient income demonstrates your ability to repay the loan.

- Savings and Assets: Having a financial safety net shows you can handle unexpected expenses while making mortgage payments.

- Property Type and Location: Loan terms and eligibility might vary based on the property type (e.g., single-family, condo) and its location.

2. Lender assessment process:

Lenders assess your eligibility through a pre-approval process, typically involving:

- Credit Report Review: Examining your credit history for delinquencies, defaults, and overall credit health.

- Income Verification: Reviewing paystubs, tax returns, and other documents to confirm your income and employment status.

- Debt Verification: Verifying your existing debts and calculating your DTI ratio.

- Asset Verification: Reviewing bank statements and other documents to confirm your savings and assets.

- Property Valuation: Assessing the value of the property you intend to purchase.

3. Financial metrics and ratios:

- Credit Score: Different lenders have minimum credit score requirements, often ranging from 620 to 740+.

- DTI Ratio: Most lenders prefer DTIs below 36%, but some may accept higher ratios with compensating factors like strong credit scores.

- Loan-to-Value Ratio (LTV): This compares the loan amount to the property value. Higher down payments result in lower LTVs, making the loan more attractive to lenders.

4. Improving your eligibility:

- Build and maintain a good credit score: Pay bills on time, manage debt wisely, and avoid unnecessary credit inquiries.

- Reduce your DTI ratio: Pay off existing debts or increase your income to improve your debt-to-income ratio.

- Save for a larger down payment: Having a larger down payment reduces the loan amount and LTV, making you a more attractive borrower.

- Maintain stable employment: Consistent employment with sufficient income demonstrates your ability to repay the loan.

- Seek guidance from a mortgage professional: They can help you understand your eligibility, recommend strategies, and guide you through the loan application process.

5. Credit history's role:

Credit history plays a crucial role in mortgage eligibility and approval. A good credit score demonstrates your responsible financial behavior and reduces the lender's risk. Lower credit scores can lead to higher interest rates, stricter loan terms, or even loan denial.

Remember, these are general guidelines, and specific requirements may vary depending on the lender and loan type. Consulting a mortgage professional can provide personalized advice based on your unique financial situation.