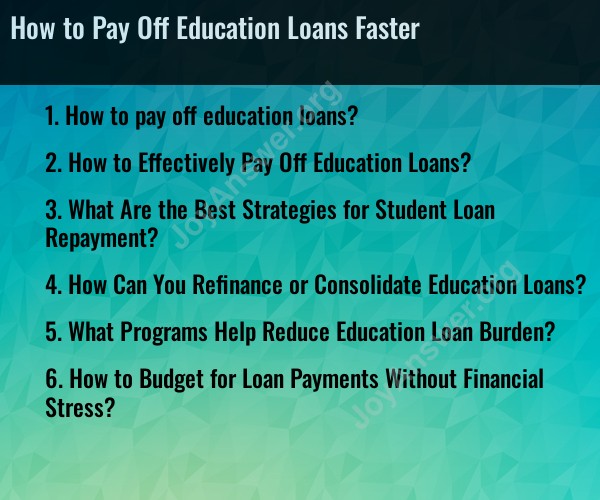

How to pay off education loans?

Paying off education loans faster comes down to strategy, discipline, and smart financial planning. Here are the most effective ways to do it:

1. Pay More Than the Minimum

The minimum keeps you in good standing but barely reduces the principal.

Even an extra $50–$100 per month can cut years off your repayment and save thousands in interest.

2. Make Biweekly Payments

Instead of one payment a month, split it in two (every two weeks).

That results in 26 half-payments (13 full payments) per year instead of 12, chipping away at the balance faster.

3. Target High-Interest Loans First (Avalanche Method)

If you have multiple loans, pay the highest interest loan more aggressively while making minimum payments on the rest.

This minimizes total interest paid.

4. Consider the Snowball Method (for Motivation)

Pay off the smallest balance first to get quick wins and build momentum.

Then roll that payment into the next loan.

5. Refinance (if you qualify)

If you have good credit and stable income, refinancing can lower your interest rate.

Be careful: refinancing federal loans means losing benefits like income-driven repayment and forgiveness programs.

6. Use Windfalls and Bonuses

Tax refunds, work bonuses, or side hustle income → direct them to extra loan payments instead of spending.

7. Automate Extra Payments

Set up autopay with an extra amount each month.

Many lenders also offer a small interest rate discount (e.g., 0.25%) for autopay.

8. Cut Expenses & Boost Income

Even temporary sacrifices (less dining out, cheaper housing, side gig earnings) can free up cash for loan payments.

Every dollar extra you throw at the loan saves future interest.

9. Check for Employer Repayment Assistance

Some employers offer student loan repayment as a benefit.

If available, combine it with your payments to accelerate progress.

10. Stay Motivated

Track your progress visually (charts, apps).

Reward yourself when you hit milestones.

✅ Example:

If you owe $30,000 at 6% interest over 10 years, your monthly payment is about $333.

Paying $450/month instead cuts repayment to ~7 years and saves over $3,700 in interest.

Education loans can be a significant hurdle, but with the right strategy, you can minimize stress and maximize your savings. This guide breaks down the best ways to tackle your education debt, from effective payment strategies to refinancing options and budgeting tips.

How to Effectively Pay Off Education Loans?

The most effective path to paying off your loans involves a strategic mix of maximizing payments and minimizing interest.

The "Avalanche" Method (Best for Saving Money): This strategy focuses on saving the most money in the long run.

Make the minimum payment on all your loans.

Put any extra money toward the loan with the highest interest rate.

Once that loan is paid off, apply that extra money to the loan with the next highest interest rate, and so on.

The "Snowball" Method (Best for Motivation): This strategy is excellent for psychological momentum.

Make the minimum payment on all your loans.

Put any extra money toward the loan with the smallest balance.

Once that loan is paid off, apply the money you were paying on it to the next smallest loan. The "snowball" of extra cash grows with each loan you eliminate.

Make Bi-Weekly Payments: By paying half of your monthly payment every two weeks, you'll end up making one extra full payment per year, significantly accelerating your payoff timeline.

What Are the Best Strategies for Student Loan Repayment?

Beyond the payoff methods, specific actions can make your repayment smoother and faster.

Pay More Than the Minimum: This is the most direct way to save money and time. Even a small amount—say, an extra $50 per month—can shave months off your loan term and save hundreds in interest.

Enroll in Auto-Pay: Many loan servicers offer a small interest rate reduction (usually 0.25%) when you set up automatic monthly payments. This also ensures you never miss a payment, avoiding late fees and credit score damage.

Keep Your Job Status Updated: If your income has dropped or you've lost your job, immediately contact your loan servicer to inquire about deferment or forbearance options to temporarily pause or reduce payments. While interest often still accrues, these can be lifesavers during financial hardship.

How Can You Refinance or Consolidate Education Loans?

Refinancing and consolidation are powerful tools for reducing your interest rate and simplifying your monthly payments.

Refinancing (Private Loans)

What it is: Replacing your existing loan(s) with a new private loan at a lower interest rate, often with a different loan servicer.

When to do it: If your credit score has significantly improved since graduation, or if you can qualify for a much lower interest rate than your current rate.

The Benefit: A lower interest rate directly translates to massive savings over the life of the loan and a faster payoff.

Consolidation (Federal Loans)

What it is: Combining multiple federal loans into a single new Direct Consolidation Loan.

The Benefit: Simplifies repayment to a single monthly bill and can give you access to flexible Income-Driven Repayment (IDR) plans. Important: Consolidation does not typically lower your interest rate; instead, it uses a weighted average of your existing rates.

What Programs Help Reduce Education Loan Burden?

Federal and state governments, as well as employers, offer several programs to reduce your total debt burden.

Public Service Loan Forgiveness (PSLF): This program forgives the remaining balance on your Direct Federal Loans after you have made 120 qualifying monthly payments while working full-time for a qualifying employer (government organizations, 501(c)(3) non-profits).

Income-Driven Repayment (IDR) Plans: These federal plans (like SAVE, PAYE, IBR) cap your monthly student loan payment at an amount affordable based on your income and family size. After 20 or 25 years of qualifying payments, any remaining balance is forgiven.

Teacher Loan Forgiveness: Teachers in low-income schools can qualify for forgiveness of up to $17,500 on their Direct Subsidized and Unsubsidized Loans.

Employer Assistance Programs: Increasingly, companies offer student loan contribution benefits as part of their compensation packages, where the employer pays a set amount toward your principal each month. Check with your HR department.

How to Budget for Loan Payments Without Financial Stress?

A proactive, realistic budget is the foundation of stress-free loan repayment.

The 50/30/20 Rule: A simple framework to guide your spending:

50% goes toward Needs (Housing, Groceries, Loan Payments, Utilities).

30% goes toward Wants (Entertainment, Dining out, Hobbies).

20% goes toward Savings and Debt Payoff (Extra Principal).

Find "Hidden" Money: Go through your credit card statements and bank accounts to find recurring subscriptions you don't use (streaming services, gym memberships) and cancel them. Dedicate that savings directly to your loan principal.

Create a Buffer Fund: Instead of building a full emergency fund first, set aside one month's worth of loan payments in an easily accessible savings account. This acts as a buffer against unexpected expenses, preventing you from having to choose between missing a loan payment and covering an essential bill.

By implementing these strategies, you can take control of your student loans and work toward financial freedom sooner.