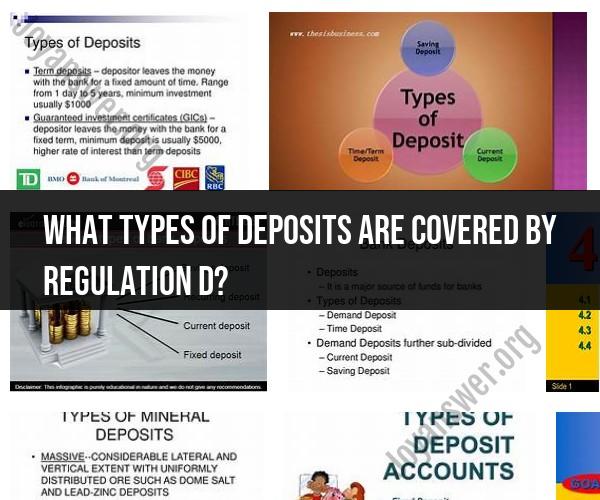

What types of deposits are covered by Regulation D?

Regulation D is a federal regulation in the United States that imposes certain reserve requirements and transaction limitations on certain types of deposit accounts held at financial institutions. It primarily applies to deposits at banks and credit unions. Regulation D defines three main types of deposits and places transaction limitations on two of them. Here are the types of deposits covered by Regulation D:

Demand Deposits: These are also known as non-interest-bearing transaction accounts. They include checking accounts and similar types of deposit accounts where depositors can make an unlimited number of transactions, such as withdrawals and transfers, without restrictions. Regulation D does not place any transaction limitations on demand deposits.

Savings Deposits: These are often referred to as regular savings accounts or passbook savings accounts. Regulation D places transaction limitations on savings deposits. Specifically, it limits you to a maximum of six preauthorized transfers or withdrawals per month. These transfers or withdrawals can include automatic transfers, telephone transfers, online transfers, and checks or debit card payments made from the savings account. Exceeding this limit can result in penalties or the account being reclassified by the financial institution.

Time Deposits: These are certificates of deposit (CDs) and other term deposit accounts with fixed maturities. Regulation D generally does not impose transaction limitations on time deposits because these accounts are intended to be held for a fixed period, and early withdrawals may result in penalties.

It's important to note that while Regulation D imposes transaction limits on savings deposits, it does not specify interest rate requirements. The interest rate you earn on a savings deposit is determined by your financial institution and the terms of the account.

Regulation D was established by the Federal Reserve to help maintain the stability of financial institutions and their ability to meet the demands of depositors. It's important for account holders to be aware of the transaction limits imposed by Regulation D on their savings deposits to avoid any potential penalties or disruptions in their banking activities. Additionally, these regulations can change over time, so it's a good practice to check with your financial institution for the most up-to-date information regarding your specific deposit accounts.