What is a consumer account under Regulation DD?

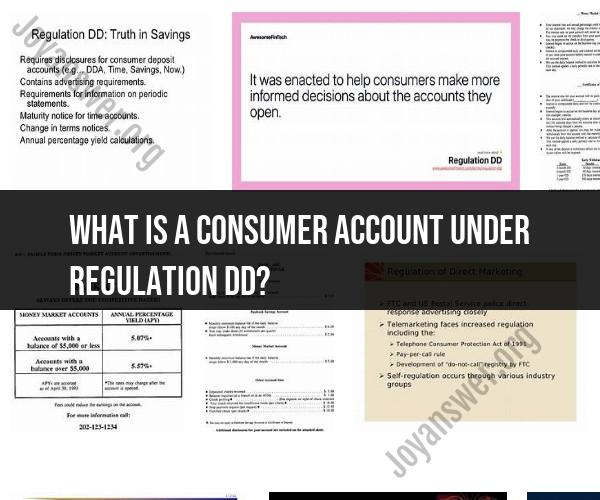

Under Regulation DD, which is part of the Truth in Savings Act, a consumer account is a deposit account held by an individual primarily for personal, family, or household purposes. Regulation DD establishes disclosure requirements for financial institutions regarding the terms and conditions of deposit accounts offered to consumers. These disclosures are intended to provide consumers with clear and comprehensive information about their accounts, including interest rates, fees, and terms, to help them make informed decisions about where to deposit their money.

Here are some key points related to consumer accounts under Regulation DD:

Personal, Family, or Household Purposes: Consumer accounts are accounts that individuals use for their personal financial needs, such as savings accounts, checking accounts, certificates of deposit (CDs), and other deposit products. These accounts are not intended for businesses or commercial purposes.

Disclosure Requirements: Financial institutions are required to provide specific disclosures to consumers when they open or maintain consumer accounts. These disclosures include information about interest rates, fees, account terms, and any special features associated with the account.

Annual Percentage Yield (APY): Regulation DD requires financial institutions to prominently disclose the annual percentage yield (APY) on consumer deposit accounts. The APY represents the effective annual rate of return, taking into account compounding of interest.

Fee Disclosures: Financial institutions must disclose any fees associated with the account, such as monthly maintenance fees, overdraft fees, ATM fees, and other charges that may apply.

Terms and Conditions: Consumers must be provided with clear information about the terms and conditions of their accounts, including withdrawal restrictions, minimum balance requirements, and any penalties for early withdrawal or account closure.

Periodic Statements: Financial institutions are typically required to provide periodic account statements to consumers, summarizing account activity and disclosing certain information about the account, including interest earned and fees charged.

Changes in Terms: Regulation DD also specifies the procedures that financial institutions must follow when making changes to the terms of consumer accounts. These procedures include advance notice to consumers before implementing changes.

Enforcement: Regulatory agencies, such as the Consumer Financial Protection Bureau (CFPB), oversee compliance with Regulation DD and may take enforcement actions against financial institutions that do not comply with the disclosure requirements.

The primary goal of Regulation DD is to promote transparency and ensure that consumers have access to clear and accurate information about their deposit accounts. This helps consumers make informed decisions about where to deposit their money and allows them to compare account offerings from different financial institutions more effectively.