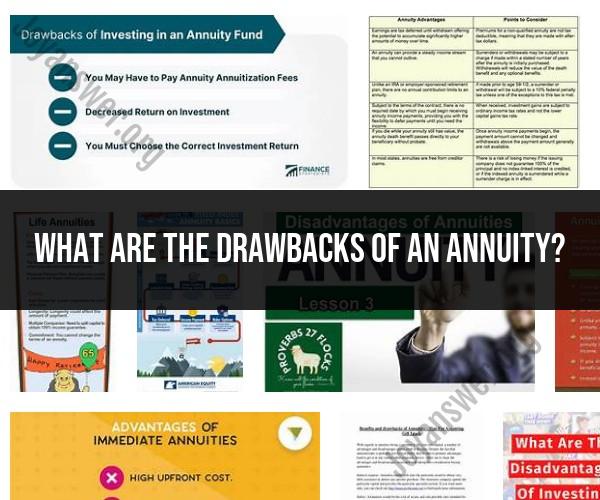

What are the drawbacks of an annuity?

While annuities can provide valuable financial benefits for some individuals, they also come with several potential drawbacks that you should consider before purchasing one. Here are some common drawbacks of annuities:

Lack of Liquidity:

- Annuities are typically designed for the long term and may come with restrictions on accessing your money. With some annuity types, early withdrawals can result in surrender charges and penalties, potentially eroding your principal.

Complexity:

- Annuities can be complex financial products with various options and fees. Understanding the terms and features of the annuity you're considering can be challenging, making it important to thoroughly review the contract.

Fees and Expenses:

- Annuities often have fees and expenses, which can include management fees, administrative charges, mortality and expense (M&E) fees, and surrender charges. These costs can eat into your returns over time.

Limited Investment Options:

- Some annuities, particularly fixed annuities, offer limited investment options compared to other retirement accounts like IRAs or 401(k)s. If you prefer more control over your investments, this can be a drawback.

Potential for Lower Returns:

- The returns on annuities, especially fixed and immediate annuities, may be lower than what you could earn by investing in other financial instruments like stocks and bonds. Annuities prioritize safety and predictability over the potential for higher returns.

Inflexibility:

- Once you purchase an annuity, you typically have limited flexibility to change the terms or access your funds. This lack of flexibility may not suit your changing financial needs or goals.

No Inflation Protection:

- Many annuities do not provide inflation protection, meaning the purchasing power of your annuity payments may erode over time due to rising prices.

Loss of Control:

- When you buy an annuity, you surrender control of a portion of your assets to the insurance company. This lack of control can be a drawback if you prefer to manage your investments actively.

Tax Implications:

- Depending on the type of annuity, the income you receive may be taxable. If you're in a high tax bracket, this can impact the after-tax income you receive from the annuity.

Not Ideal for Short-Term Needs:

- Annuities are typically not suitable for short-term financial goals or emergencies due to their long-term nature and potential penalties for early withdrawals.

Loss of Principal:

- In some annuity types, such as variable annuities, there is a risk of losing part or all of your principal if your investments within the annuity perform poorly.

Complex Payout Structures:

- Some annuities have complex payout structures, including multiple options for how and when you receive income. Understanding these options can be challenging.

High Commissions:

- Some financial advisors and insurance agents earn high commissions when selling annuities, which can create a conflict of interest and potentially lead to recommendations that may not be in your best financial interest.

It's crucial to carefully evaluate your financial goals, risk tolerance, and individual circumstances before purchasing an annuity. Additionally, consider seeking advice from a financial advisor who can provide personalized guidance and help you determine whether an annuity aligns with your overall retirement and financial plan.