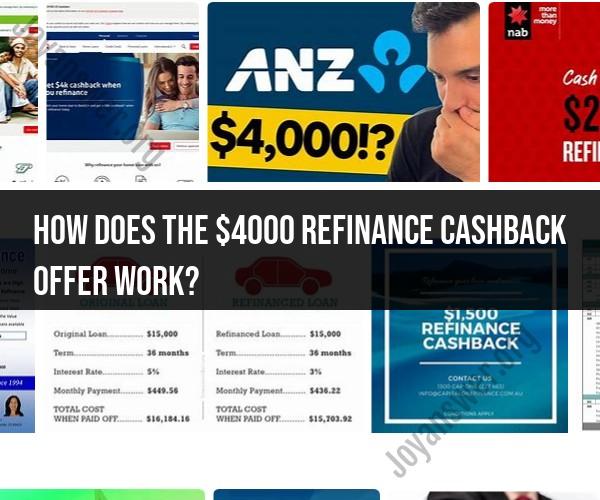

How does the $4000 refinance cashback offer work?

The $4000 refinance cashback offer is a financial incentive provided by some lenders to encourage borrowers to refinance their existing mortgages. While the specific terms and conditions may vary depending on the lender, here's a general overview of how such an offer typically works:

Eligibility: Lenders will specify eligibility criteria for the cashback offer. Common criteria may include a minimum loan amount, a minimum credit score, and the type of mortgage being refinanced (e.g., primary residence, investment property).

Application: To take advantage of the cashback offer, you need to apply for mortgage refinancing with the lender offering the promotion. During the application process, you'll need to provide documentation and go through the underwriting process as with any mortgage application.

Loan Approval: Once your application is approved, you'll proceed with the refinance process, which involves paying off your existing mortgage with the new loan. This may include closing costs and fees associated with the refinance.

Cashback Disbursement: After the refinance is complete and the new mortgage is funded, the lender will disburse the cashback incentive to you. This is typically done shortly after the loan closes.

Use of Cashback: The cashback amount is yours to use as you see fit. Many borrowers use it to cover expenses related to the refinance, such as closing costs, prepayment of property taxes or insurance, or even home improvements. It can also be used for other financial needs.

Repayment: In most cases, the cashback offer is not a loan but a promotional incentive. You are not required to repay the cashback amount to the lender. However, if you choose to refinance again or pay off the new mortgage within a specific timeframe, you may be required to repay a portion or all of the cashback.

Terms and Conditions: Be sure to carefully read and understand the terms and conditions of the cashback offer, as they may vary from lender to lender. Pay attention to any restrictions, timeframes, or special requirements associated with the offer.

It's important to note that while a cashback offer can be enticing, it should not be the sole factor in your decision to refinance. Consider the overall terms of the new mortgage, including the interest rate, loan term, and total costs, to determine if refinancing is financially beneficial for your situation.

Before proceeding with any mortgage refinance, it's advisable to compare offers from multiple lenders, thoroughly review the terms and conditions, and calculate the potential savings or costs associated with the refinance. Consulting with a financial advisor or mortgage professional can also help you make an informed decision.