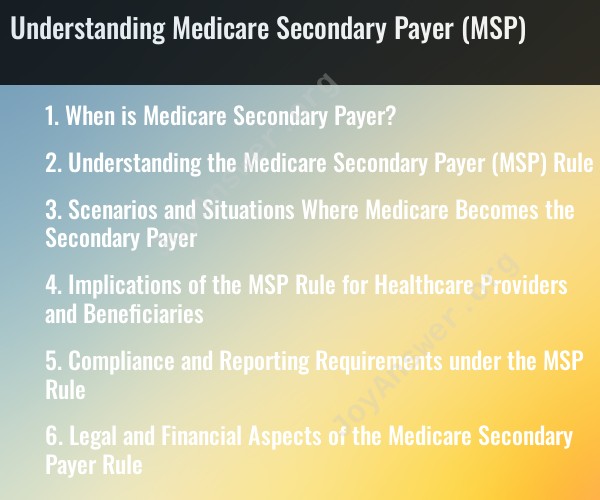

When is Medicare Secondary Payer?

Medicare Secondary Payer (MSP) is a set of rules and provisions that determine when Medicare may pay for healthcare services as a secondary payer, in addition to other forms of insurance. Medicare serves as the primary payer in many situations, but there are instances where it becomes the secondary payer. Here are some common scenarios in which Medicare becomes the secondary payer:

Employer-Sponsored Group Health Plans: If you are 65 or older and are covered by an employer-sponsored group health plan, and the employer has 20 or more employees, your group health plan is usually the primary payer, and Medicare becomes secondary.

End-Stage Renal Disease (ESRD) with Group Health Insurance: If you have ESRD and have group health insurance through your current employment or the employment of a family member, Medicare may be the secondary payer for the first 30 months of your Medicare entitlement. After that period, Medicare becomes the primary payer.

Workers' Compensation: If you have a work-related injury or illness that is covered by workers' compensation, workers' compensation is the primary payer, and Medicare becomes the secondary payer for healthcare related to the injury or illness.

No-Fault Insurance: In some cases, Medicare may be the secondary payer when a person is involved in an automobile accident or another incident covered by a no-fault insurance policy.

Medicaid: If you are eligible for both Medicare and Medicaid (dual eligible), Medicaid may cover costs that Medicare doesn't, such as premiums, deductibles, and cost-sharing, making Medicaid the secondary payer.

Medicare Supplement Insurance (Medigap): If you have both Medicare and a Medigap policy, the Medigap policy may cover costs not paid by Medicare, such as copayments, coinsurance, and deductibles, making Medigap the secondary payer.

Liability Insurance: In cases involving liability insurance, such as when someone else is responsible for your injury or illness (e.g., a personal injury lawsuit), Medicare may be the secondary payer. This is to ensure that the liable party's insurance pays before Medicare.

Voluntary Medicare Set-Aside Arrangements (MSAs): In some cases, individuals may establish MSAs to allocate a portion of their settlement funds to cover future medical expenses related to their injury. Medicare may be the secondary payer in such situations.

It's important to note that Medicare Secondary Payer rules are complex and subject to change. The goal is to ensure that Medicare does not pay for services when another form of insurance or a responsible third party is legally responsible for payment. If you are eligible for Medicare and have other insurance coverage, it's essential to understand the coordination of benefits to avoid complications and ensure that your healthcare expenses are appropriately covered. Consulting with your insurance provider, healthcare provider, or a Medicare expert can help clarify your specific situation.

Understanding the Medicare Secondary Payer (MSP) Rule

The Medicare Secondary Payer (MSP) rule is a complex set of regulations that determine which payer is responsible for paying for healthcare services provided to Medicare beneficiaries. Under the MSP rule, Medicare is the secondary payer for many types of healthcare coverage, including employer-sponsored health insurance, workers' compensation, and liability insurance.

Scenarios and Situations Where Medicare Becomes the Secondary Payer

Medicare becomes the secondary payer in a number of situations, including:

- When a Medicare beneficiary has another type of health insurance, such as employer-sponsored health insurance or coverage through a spouse's employer.

- When a Medicare beneficiary is injured on the job and is entitled to workers' compensation benefits.

- When a Medicare beneficiary is injured in an accident and is entitled to liability insurance benefits.

- When a Medicare beneficiary is receiving certain types of government assistance, such as Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI).

Implications of the MSP Rule for Healthcare Providers and Beneficiaries

Healthcare providers and beneficiaries must be aware of the MSP rule in order to avoid billing errors and financial penalties.

Healthcare providers are responsible for determining whether Medicare is the primary or secondary payer for a Medicare beneficiary's services. If Medicare is the secondary payer, the healthcare provider must bill the primary payer first. If the healthcare provider bills Medicare first, Medicare may deny the claim and the healthcare provider may be responsible for collecting the full cost of services from the beneficiary.

Medicare beneficiaries are responsible for providing their healthcare providers with accurate information about their health insurance coverage. If a Medicare beneficiary fails to provide their healthcare provider with accurate information, the beneficiary may be responsible for paying for services that Medicare would have covered.

Compliance and Reporting Requirements under the MSP Rule

Healthcare providers and beneficiaries must comply with a number of reporting requirements under the MSP rule.

Healthcare providers must report certain types of payments to Medicare. For example, healthcare providers must report payments from workers' compensation and liability insurance companies.

Medicare beneficiaries must report certain changes in their health insurance coverage to Medicare. For example, Medicare beneficiaries must report if they start or stop working, or if they change their employer-sponsored health insurance plan.

Legal and Financial Aspects of the Medicare Secondary Payer Rule

The MSP rule is a complex set of regulations with a number of legal and financial implications.

Healthcare providers should consult with an attorney to ensure that they are in compliance with the MSP rule. Healthcare providers may also want to consider purchasing liability insurance to protect themselves from financial losses in the event that they are sued for MSP billing errors.

Medicare beneficiaries should contact Medicare if they have any questions about the MSP rule or their responsibilities under the rule. Medicare beneficiaries may also want to consult with an attorney if they have any concerns about their MSP coverage.

Conclusion

The MSP rule is a complex set of regulations that determine which payer is responsible for paying for healthcare services provided to Medicare beneficiaries. Healthcare providers and beneficiaries must be aware of the MSP rule in order to avoid billing errors and financial penalties.