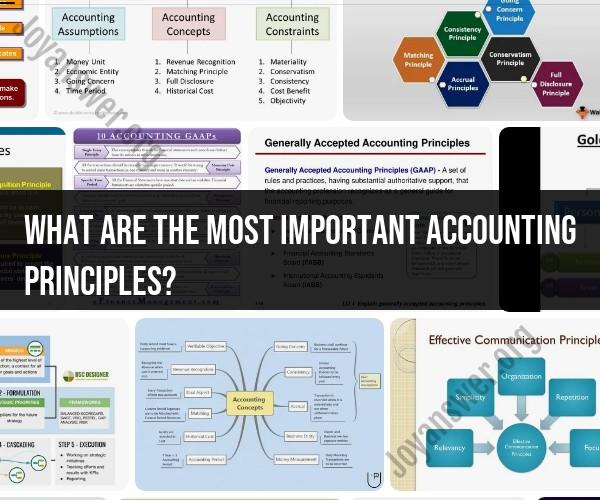

What are the most important accounting principles?

Accounting principles, also known as Generally Accepted Accounting Principles (GAAP) in the United States, provide a framework for financial reporting and ensure consistency and transparency in financial statements. There are several important accounting principles that serve as the foundation for financial reporting. Here are some of the most important ones:

Accrual Basis of Accounting: Under this principle, revenue is recognized when it is earned, and expenses are recognized when they are incurred, regardless of when cash is received or paid. This principle helps provide a more accurate picture of a company's financial performance.

Going Concern Principle: This principle assumes that a business will continue to operate indefinitely unless there is evidence to the contrary. It allows assets and liabilities to be valued based on the assumption of ongoing operations.

Consistency: This principle requires a company to use the same accounting methods and principles from one period to the next. Consistency enhances comparability between financial statements over time.

Materiality: Financial statements should disclose all relevant information that could influence the decisions of financial statement users. However, immaterial items need not be disclosed to avoid excessive detail in financial reporting.

Conservatism (Prudence): This principle suggests that when there are uncertainties or choices regarding the recognition of revenue or the valuation of assets, a conservative approach should be taken. This means recognizing expenses and liabilities sooner rather than later and recognizing revenue only when it is reasonably certain.

Historical Cost Principle: Assets are typically recorded on the balance sheet at their original acquisition cost, rather than at their current market value. This principle provides a reliable and verifiable basis for recording assets.

Matching Principle: This principle dictates that expenses should be matched with the revenue they help generate. In other words, expenses should be recognized in the same accounting period as the related revenue.

Full Disclosure: Financial statements should provide all necessary information to understand the financial position and performance of an organization. This includes footnotes, supplementary schedules, and other disclosures that provide additional context and detail.

Revenue Recognition Principle: This principle outlines when and how revenue should be recognized. It requires revenue to be recognized when it is earned and realized or realizable, and when it can be measured with reasonable reliability.

Consolidation: For entities with subsidiaries or investments in other companies, the consolidation principle requires the financial statements to present the combined financial results of the parent and its subsidiaries to provide a true and fair view of the group's financial position and performance.

These accounting principles collectively ensure that financial statements are prepared consistently, accurately, and transparently, making them useful for decision-making by investors, creditors, and other stakeholders. It's important to note that while these principles are fundamental, there may be specific industry or regional variations in accounting standards and regulations that need to be considered. Additionally, accounting standards can evolve over time, so it's essential for businesses to stay updated with the latest accounting guidance and regulations relevant to their operations.

The Fundamental Accounting Principles You Should Know

The fundamental accounting principles are the basic guidelines that accountants follow when recording and reporting financial information. These principles are essential for ensuring that financial statements are accurate and reliable.

Some of the most important fundamental accounting principles include:

- Revenue recognition principle: Revenue should be recognized when it is earned and realized.

- Expense recognition principle: Expenses should be recognized when they are incurred.

- Matching principle: Expenses should be matched with the revenues they generate.

- Accrual principle: Financial statements should be prepared on the assumption that the business will continue to operate in the foreseeable future.

- Going concern principle: Assets and liabilities should be recorded at their fair market value.

Key Accounting Principles: Building Blocks of Financial Reporting

The key accounting principles are the foundation of financial reporting. These principles are used to record and report financial information in a way that is consistent and comparable across different businesses.

Some of the most important key accounting principles include:

- Cost principle: Assets and liabilities should be recorded at their cost.

- Objectivity principle: Financial statements should be prepared based on objective evidence.

- Consistency principle: Businesses should use the same accounting methods over time.

- Materiality principle: Only material transactions and events should be recorded in the financial statements.

- Full disclosure principle: All material information about a business's financial condition and performance should be disclosed in the financial statements.

Understanding and Applying Important Accounting Standards

Accounting standards are the rules and regulations that govern how financial information is recorded and reported. These standards are developed by accounting organizations such as the Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB).

It is important for accountants to understand and apply accounting standards correctly. This is because accounting standards help to ensure that financial statements are accurate, reliable, and comparable across different businesses.

Some of the most important accounting standards include:

- Generally Accepted Accounting Principles (GAAP): GAAP is the accounting framework that is used by businesses in the United States.

- International Financial Reporting Standards (IFRS): IFRS is the accounting framework that is used by businesses in many countries outside of the United States.

- Industry-specific accounting standards: Some industries have their own specific accounting standards. For example, the insurance industry has its own set of accounting standards that are developed by the Accounting for Insurance Liabilities (OIL) Committee.

By understanding and applying important accounting principles and standards, accountants can help to ensure that financial statements are accurate, reliable, and informative.