What is the difference between managerial and government accounting?

Accounting plays a critical role in organizations, ensuring accurate financial records and informed decision-making. Two prominent branches of accounting are managerial accounting and government accounting. Let's delve into the distinctions between these two fields:

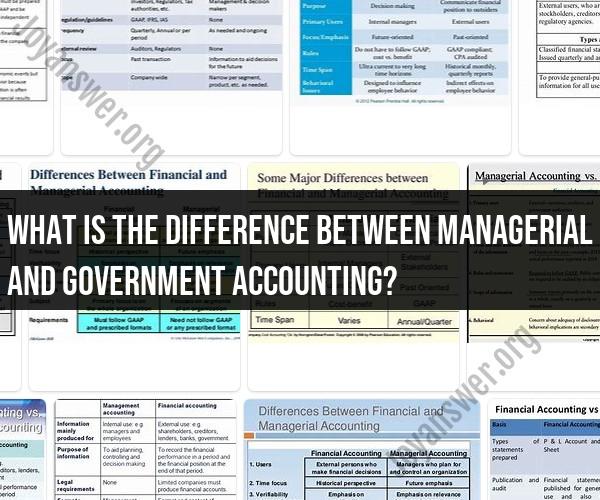

Managerial Accounting:

Managerial accounting, also known as cost accounting, focuses on providing internal information to support management's decision-making process. Key characteristics of managerial accounting include:

- Internal Use: Managerial accounting information is used internally by managers and executives to make strategic decisions, set budgets, and evaluate performance.

- Future-Oriented: Managerial accounting emphasizes planning for the future. It involves forecasting, budgeting, and identifying cost-effective strategies.

- Cost Analysis: Managers analyze costs related to production, distribution, and other business activities to determine pricing strategies and optimize profitability.

- Flexibility: Managerial accounting allows for customization of reports and analysis to address specific management needs and scenarios.

Government Accounting:

Government accounting focuses on financial management and reporting in the public sector. This includes government entities at various levels, such as federal, state, and local governments. Key features of government accounting include:

- Public Accountability: Government accounting serves the public interest by providing transparency and accountability in the use of public funds and resources.

- Legal Compliance: Government accountants adhere to specific accounting standards and regulations tailored to the public sector, ensuring compliance with laws and regulations.

- Fund Accounting: Government accounting often uses fund-based accounting to track financial resources allocated for specific purposes, such as education, infrastructure, or public safety.

- Reporting Requirements: Government entities are required to publish financial statements and reports to communicate financial status and performance to the public.

Comparing the Two:

While both managerial and government accounting focus on financial information, their primary audiences, objectives, and methodologies differ significantly. Managerial accounting is geared towards internal decision-making, whereas government accounting serves the public interest and regulatory compliance.

Conclusion:

Distinguishing between managerial and government accounting is essential for understanding the roles and responsibilities of accountants in different contexts. Each field serves distinct purposes and contributes to effective financial management, whether it's optimizing business operations or ensuring transparency in public financial affairs.