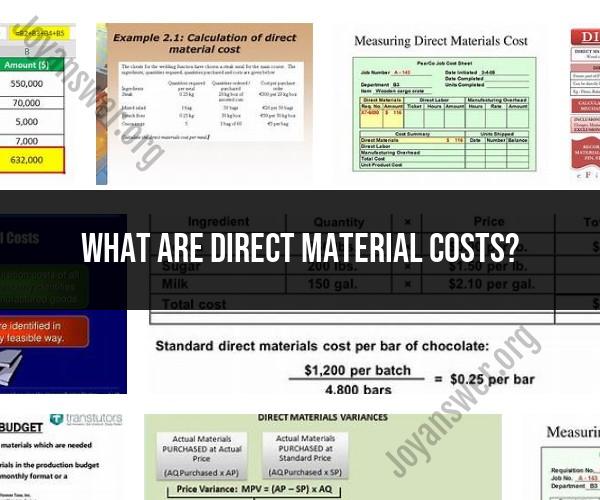

What are direct material costs?

Direct material costs, often referred to simply as "material costs," are a type of manufacturing cost incurred by a company during the production of goods. These costs specifically represent the expenses associated with the raw materials and components that are directly used in the manufacturing process to create a product. Direct material costs are a key component of a company's overall cost of goods sold (COGS) and are essential for calculating the total cost of production.

Here are the main components and characteristics of direct material costs:

Raw Materials: Direct material costs encompass the expenses incurred for the raw materials used in the production process. Raw materials can include items like wood, metal, plastic, fabric, chemicals, or any other materials that go into making the product.

Direct Usage: To qualify as a direct material cost, the material must be used directly in the production process. This means that the material is an integral part of the final product, and its consumption can be traced directly to the production of a specific unit or batch.

Measurable: Direct material costs are typically measured in physical quantities, such as pounds, kilograms, liters, or other units relevant to the specific materials being used. This allows for accurate tracking of the amount of material consumed.

Variable Cost: Direct material costs are considered variable costs because they vary in direct proportion to the level of production. As production increases, so do the direct material costs, and vice versa.

Direct vs. Indirect Materials: It's important to distinguish between direct and indirect materials. Direct materials are used in the actual manufacturing process and are a direct cost of producing goods. Indirect materials, on the other hand, are materials used in the production process but are not traceable to specific units of production. Indirect materials are considered part of overhead costs.

Direct material costs play a crucial role in calculating the cost of goods sold (COGS) on a company's income statement. They are also used in determining the cost of inventory on the balance sheet. Accurate tracking and management of direct material costs are essential for cost control, pricing decisions, and overall financial management within a manufacturing or production-oriented business.

To calculate direct material costs for a specific production run, you multiply the quantity of each type of raw material used by its unit cost and then sum up these individual costs to get the total direct material cost for that production batch or period.