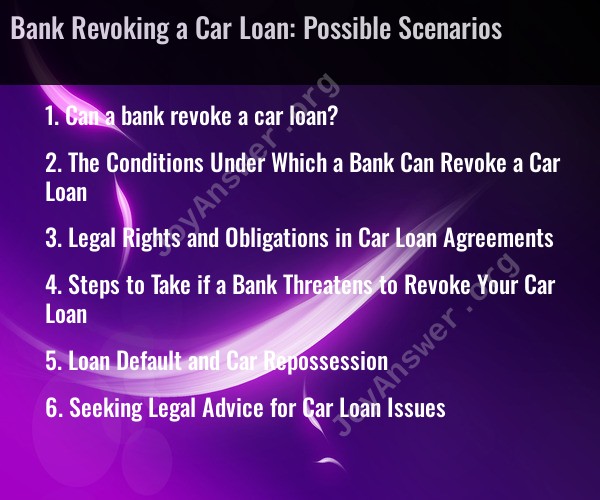

Can a bank revoke a car loan?

Banks and financial institutions typically have the ability to revoke or cancel a car loan under specific circumstances, but it's not a decision they take lightly. The conditions under which a bank might revoke a car loan can vary, and it's crucial to review the terms and conditions of your specific loan agreement to understand your rights and obligations. Here are some possible scenarios in which a bank could revoke a car loan:

Failure to Meet Loan Conditions: If you, as the borrower, fail to meet the conditions set forth in the loan agreement, the bank may have the right to revoke the loan. Common conditions include making regular, on-time payments, maintaining insurance coverage on the vehicle, and keeping the vehicle in good condition.

Misrepresentation or Fraud: If the bank discovers that you provided false or misleading information during the loan application process, such as inflating your income or providing incorrect personal information, they may have grounds to revoke the loan.

Default on Payments: If you consistently fail to make payments on the car loan, the bank may initiate the repossession process, which could lead to the revocation of the loan agreement. Most loan agreements allow the bank to repossess the vehicle if you default on payments.

Insurance Lapses: Car loans typically require the borrower to maintain appropriate insurance coverage on the vehicle. If you allow the insurance to lapse, the bank may consider this a breach of the loan agreement, which could result in revocation.

Bankruptcy: If you file for bankruptcy, it may impact the status of your car loan. The bank may seek to revoke the loan if it determines that the bankruptcy filing affects the collateral (the car) or your ability to meet the terms of the loan.

Change in Ownership: In some cases, if you transfer ownership of the vehicle to another party without the bank's consent, it could be considered a breach of the loan agreement, potentially leading to revocation.

It's important to note that the process and legal requirements for revoking a car loan can vary by jurisdiction and by the terms specified in your loan agreement. Before a bank can revoke a car loan, they often must follow specific legal procedures, including providing notice to the borrower and an opportunity to cure the default.

If you are facing difficulties with your car loan or believe the bank is attempting to revoke it, it's advisable to consult with a legal or financial professional who can provide guidance specific to your situation and the applicable laws in your jurisdiction.

The Conditions Under Which a Bank Can Revoke a Car Loan

A bank can revoke a car loan if the borrower breaches the terms of the loan agreement. These terms can include:

Failing to make payments on time: This is the most common reason for car loan revocation. If you miss a payment, the bank will typically send you a notice of delinquency. If you continue to miss payments, the bank may repossess your car.

Not maintaining adequate insurance: You are required to carry comprehensive and collision insurance on your car until you have paid off the loan. If you let your insurance lapse, the bank may revoke your loan.

Using the car for illegal purposes: If you use your car for illegal purposes, such as transporting drugs or committing crimes, the bank may revoke your loan.

Damaging the car beyond repair: If you damage your car beyond repair, the bank may revoke your loan.

Legal Rights and Obligations in Car Loan Agreements

When you sign a car loan agreement, you enter into a legal contract with the bank. This contract outlines your rights and obligations as a borrower.

Your rights as a borrower include:

The right to receive a copy of your loan agreement

The right to know the interest rate and terms of your loan

The right to make payments on time and avoid late fees

The right to dispute any errors on your account

The right to redeem your car if it is repossessed

Your obligations as a borrower include:

Making payments on time

Maintaining adequate insurance

Keeping the car in good condition

Not using the car for illegal purposes

Notifying the bank of any changes to your address or contact information

Steps to Take if a Bank Threatens to Revoke Your Car Loan

If your bank threatens to revoke your car loan, it is important to take action immediately. Here are some steps you can take:

Contact the bank: Call the bank and speak to a representative about the situation. Ask them to explain why they are threatening to revoke your loan and what you can do to prevent it.

Make a payment plan: If you are behind on payments, work with the bank to create a payment plan that you can afford.

Refinance your loan: If you have good credit, you may be able to refinance your loan with a different bank at a lower interest rate. This could make your payments more affordable and help you keep your car.

Seek legal advice: If you are unsure of your options, you should consult with an attorney. An attorney can help you understand your legal rights and obligations and advise you on the best course of action.

Loan Default and Car Repossession

If you default on your car loan, the bank has the right to repossess your car. This means that they can take your car back and sell it to recoup their losses.

The bank must follow certain procedures before repossessing your car. They must:

Give you written notice of the repossession

Provide you with an opportunity to cure the default

Reimburse you for any excess funds from the sale of your car

Seeking Legal Advice for Car Loan Issues

If you are having problems with your car loan, it is important to seek legal advice. An attorney can help you understand your legal rights and options and represent you in court if necessary.

Here are some resources that can help you find legal aid:

The Legal Services Corporation (LSC): https://www.lsc.gov/

The American Bar Association (ABA): https://www.americanbar.org/

The National Association of Consumer Bankruptcy Attorneys (NACBA): https://nacba.org/