What are the ten principles of Economics?

The "Ten Principles of Economics" are foundational concepts introduced by economist Gregory Mankiw in his book "Principles of Economics." These principles provide a framework for understanding how individuals and societies make decisions regarding the allocation of resources. Here are the ten principles:

People Face Trade-offs:

- Due to scarcity, individuals and societies must make choices. When resources are used for one purpose, they are not available for another. Trade-offs involve giving up something to obtain something else.

The Cost of Something is What You Give Up to Get It (Opportunity Cost):

- The opportunity cost of a decision is the value of the next best alternative forgone. Every choice involves sacrificing the potential benefits of the next best option.

Rational People Think at the Margin:

- Rational decision-makers weigh the additional benefit of a small change against the additional cost. This principle helps explain how individuals make decisions based on marginal (incremental) changes.

People Respond to Incentives:

- Individuals and firms respond to incentives—positive or negative. Changes in costs or benefits influence behavior and decision-making.

Trade Can Make Everyone Better Off:

- Through specialization and trade, individuals and nations can benefit by focusing on what they do best and exchanging goods and services. Trade allows for a more efficient use of resources.

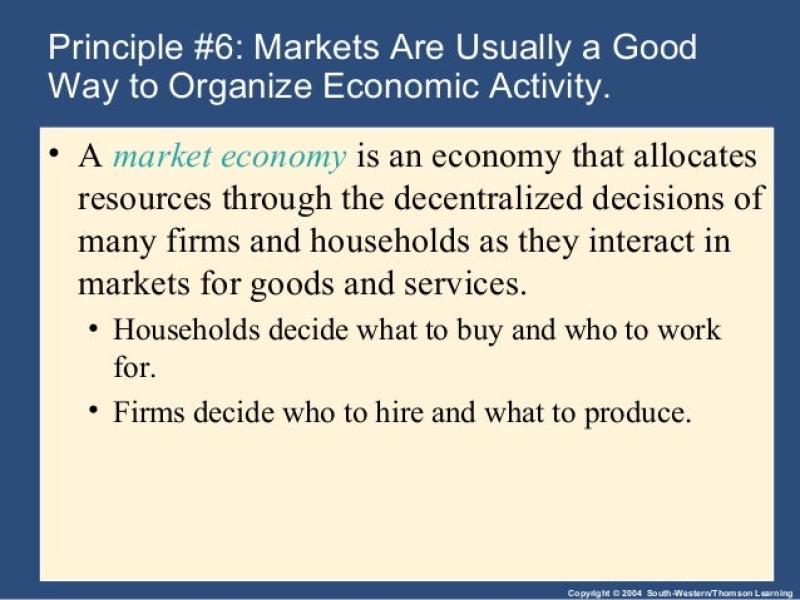

Markets Are Usually a Good Way to Organize Economic Activity:

- In a market economy, decentralized decision-making through supply and demand in markets tends to allocate resources efficiently. Prices serve as signals that guide individuals and firms in their decisions.

Governments Can Sometimes Improve Market Outcomes:

- While markets are generally effective, there are situations where government intervention can improve outcomes. Examples include enforcing property rights, ensuring competition, and addressing externalities.

A Country's Standard of Living Depends on Its Ability to Produce Goods and Services:

- The productivity of a nation's workers determines its standard of living. Productivity is influenced by technology, education, and other factors that enhance the efficiency of production.

Prices Rise When the Government Prints Too Much Money (Inflation):

- In the long run, the overall level of prices in an economy tends to increase when the government creates excessive amounts of money. This is a general statement about the relationship between money supply and inflation.

Society Faces a Short-Run Trade-off Between Inflation and Unemployment:

- In the short run, policies that lower inflation may lead to higher unemployment and vice versa. This reflects the Phillips curve trade-off between inflation and unemployment.

These principles are designed to provide a broad understanding of economic decision-making and behavior. They serve as a starting point for individuals studying economics and are often used as a foundation for introductory courses in the subject. Keep in mind that these principles provide a simplified framework and that economic analysis can become more complex as individuals delve deeper into specific economic theories and models.

What are the tenets or fundamental principles of Economics?

当然,以下是没有图片的英文版本:

What are the tenets or fundamental principles of Economics?

Economics, as a vast and multifaceted discipline, does not have a single, universally accepted set of tenets or fundamental principles. Different schools of thought and economic theories emphasize various aspects and approaches to understanding human behavior and resource allocation. However, some core ideas underpin a significant portion of economic analysis, serving as foundational pillars for exploring economic phenomena.

Here are some of the central principles you'll encounter across various economic frameworks:

Scarcity and Choice: Resources are limited, and individuals, households, and firms must make choices about how to allocate those resources to fulfill their needs and wants. This fundamental reality necessitates trade-offs between different options, forming the basis of many economic models.

Incentives and Optimization: People respond to incentives, and their actions are often driven by the desire to maximize their own benefit (utility) given the resources and constraints they face. Understanding how incentives shape behavior is crucial for predicting economic outcomes, such as market responses to price changes or individual investment decisions.

Markets and Exchange: Markets provide a mechanism for exchange and interaction between buyers and sellers, leading to the allocation of resources based on supply and demand. Analyzing market forces and their impact on prices, production, and consumption is a major pillar of economic theory.

Efficiency and Trade: Specialization and trade can increase overall efficiency and welfare by allowing individuals and economies to focus on their comparative advantages and exchange goods and services at mutually beneficial terms. This principle highlights the potential gains from international trade and economic cooperation.

Growth and Development: Understanding the factors that drive economic growth and development, such as technological advancements, institutional factors, and human capital, is a key area of focus for economists. Analyzing these elements helps formulate policies and strategies aimed at improving living standards and economic well-being.

It's important to remember that these are just some of the central principles, and their emphasis and interpretation can vary depending on the specific economic school of thought or theoretical framework being applied. Additionally, some argue that focusing on a single set of "principles" misses the richness and complexity of economic phenomena, advocating for broader perspectives that encompass social, ethical, and historical considerations.

Ultimately, understanding the diversity of ideas and assumptions under the umbrella of economics can provide a more nuanced and comprehensive perspective than relying on a limited set of principles. As you delve deeper into the field, you'll encounter various economic models and theories that utilize these core principles in different ways to explain and analyze economic phenomena.

Do you have any other questions about economic principles?