What is financial statement preparation and review audit?

Financial statement preparation and review audit involves the process of creating and examining an organization's financial statements to ensure accuracy, completeness, and compliance with accounting standards. This process is crucial for providing stakeholders, such as investors, creditors, and regulators, with reliable information about the financial health and performance of a business. Here's an overview of the key components of financial statement preparation and review audit:

Financial Statement Preparation:

Data Collection:

- Gather financial data from various sources within the organization, including accounting records, ledgers, bank statements, and supporting documentation.

Recording Transactions:

- Accountants record financial transactions in the organization's accounting system. This includes entries for revenue, expenses, assets, liabilities, and equity.

Adjustments and Accruals:

- Make necessary adjustments and accruals to ensure that financial statements reflect the economic reality of the organization. This may involve recognizing revenues and expenses that have not yet been recorded.

Financial Statement Elements:

- Prepare the primary financial statements, including:

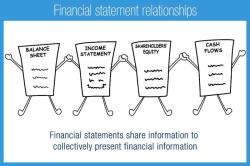

- Income Statement (Profit and Loss Statement): Reports revenues, expenses, and net income or loss over a specific period.

- Balance Sheet: Provides a snapshot of the organization's financial position, showing assets, liabilities, and equity.

- Statement of Cash Flows: Details the organization's cash inflows and outflows from operating, investing, and financing activities.

- Prepare the primary financial statements, including:

Disclosure Notes:

- Include relevant disclosure notes that provide additional information about accounting policies, contingencies, and other relevant details.

Financial Statement Review Audit:

Engagement Planning:

- Before conducting a review audit, the auditor plans the engagement, considering risk assessments, materiality, and the scope of the review.

Understanding Internal Controls:

- Gain an understanding of the organization's internal controls to assess the reliability of financial information.

Analytical Procedures:

- Perform analytical procedures to evaluate the relationships between financial statement elements and identify any unusual trends or fluctuations.

Inquiries and Substantive Procedures:

- Conduct inquiries with management and perform substantive procedures to gather evidence supporting the amounts and disclosures in the financial statements.

Documenting Findings:

- Document the auditor's findings, including any identified risks, material misstatements, or areas requiring management's attention.

Review Report:

- Provide a review report expressing limited assurance that, based on the review, the financial statements are not materially misstated. This report is less extensive than an audit opinion.

Communication with Management:

- Communicate with management regarding any issues identified during the review and work collaboratively to address concerns.

Key Differences:

Scope of Assurance:

- A review audit provides limited assurance compared to a full audit. The auditor does not express an opinion on the fairness of the financial statements but provides a conclusion that nothing has come to their attention that indicates material misstatements.

Procedures Intensity:

- A review involves fewer procedures compared to a full audit. The focus is on inquiries, analytical procedures, and obtaining limited evidence to support the financial information.

Cost and Time:

- A review is generally less costly and time-consuming than a full audit, making it a more cost-effective option for organizations that do not require a higher level of assurance.

Financial statement preparation and review audits are essential components of financial reporting, offering stakeholders insights into a company's financial position and performance while providing reasonable assurance about the accuracy of the financial information.

Financial audits play a crucial role in ensuring the reliability and integrity of financial information. They provide independent assurance to stakeholders that financial statements are accurate, complete, and prepared in accordance with established accounting standards.

1. Purpose of Financial Audits

The primary purpose of financial audits is to verify the accuracy and fairness of financial statements. This includes ensuring that:

Transactions are properly recorded and disclosed: All financial transactions should be accurately recorded in the accounting records and adequately reflected in the financial statements.

Assets and liabilities are correctly valued: Assets and liabilities should be valued in accordance with established accounting principles to represent their true financial position.

Revenues and expenses are appropriately recognized: Revenues and expenses should be recognized in the correct period and at the appropriate amounts.

2. Audit Process

The audit process involves a series of steps that auditors undertake to gather evidence and form an opinion on the fairness of financial statements. These steps typically include:

Planning and Risk Assessment: Auditors gain an understanding of the company's business, operations, and internal controls. They assess the risks of material misstatement, which are areas where there is a higher likelihood of errors or irregularities in the financial statements.

Testing Internal Controls: Auditors evaluate the effectiveness of the company's internal controls, which are processes and procedures designed to safeguard assets, prevent errors, and ensure the reliability of financial information.

Substantive Testing: Auditors perform substantive procedures to directly test the accuracy and completeness of financial data. This may include examining transactions, reviewing supporting documentation, and performing analytical procedures.

3. Audit Reports

The culmination of the audit process is the issuance of an audit report. The audit report communicates the auditor's findings and opinion to stakeholders. It includes:

Scope of the Audit: Describes the scope of the audit work performed and the limitations of the audit.

Management's Responsibility for Financial Statements: Acknowledges that management is responsible for the preparation and presentation of financial statements.

Auditor's Responsibility: Outlines the auditor's responsibility to express an opinion on the financial statements.

Auditor's Opinion: Expresses the auditor's opinion on whether the financial statements are presented fairly in all material respects in accordance with the applicable financial reporting framework.

Basis for Opinion: Explains the basis for the auditor's opinion, including the audit procedures performed and the evidence obtained.