How does credit score affect your mortgage rate?

Your credit score has a significant influence on the mortgage rate you can secure when applying for a home loan. Mortgage lenders use credit scores to assess your creditworthiness, and borrowers with higher credit scores generally receive better interest rates. Here's how your credit score affects your mortgage rate:

Credit Score Tiers: Lenders often categorize borrowers into different credit score tiers. These tiers can vary by lender but typically fall into categories like excellent, good, fair, and poor credit. Borrowers with higher credit scores fall into the "excellent" or "good" categories and are more likely to qualify for lower interest rates.

Risk Assessment: Lenders use credit scores to assess the risk associated with lending to a particular borrower. A higher credit score is seen as an indicator of responsible financial behavior, which suggests that the borrower is less likely to default on their mortgage. This reduced risk translates into lower interest rates.

Interest Rate Discounts: Many lenders offer interest rate discounts or better terms to borrowers with higher credit scores. These discounts can result in lower monthly mortgage payments and potentially save you a significant amount of money over the life of your loan.

Credit Score Thresholds: Different lenders have different credit score thresholds for their loan products. Meeting or exceeding a lender's minimum credit score requirement can open the door to better loan options and lower interest rates. However, a lower credit score may limit your loan choices and lead to higher rates.

Private Mortgage Insurance (PMI) Costs: If your credit score is on the lower end, you may be required to pay higher premiums for private mortgage insurance if you make a down payment below a certain percentage of the home's purchase price. This can increase your overall housing costs.

Negotiation: In some cases, borrowers with strong credit may be able to negotiate with lenders for even better interest rates and loan terms. If you have a high credit score, it's worth discussing potential rate reductions with your lender.

It's important to note that the specific impact of your credit score on your mortgage rate can vary from lender to lender, and market conditions can also play a role. Therefore, it's advisable to shop around and compare mortgage offers from multiple lenders to find the best mortgage rate based on your credit score and financial situation. Additionally, improving your credit score before applying for a mortgage can help you secure a more favorable interest rate and potentially save you money over the life of your loan.

Understanding the direct impact of credit scores on mortgage rates

Your credit score is a major factor that lenders consider when determining your mortgage interest rate. A higher credit score indicates to lenders that you are a responsible borrower and are more likely to repay your loan on time and in full. As a result, lenders are more likely to offer you a lower interest rate.

For example, a borrower with a credit score of 760 may qualify for a mortgage interest rate of 4%, while a borrower with a credit score of 650 may only qualify for an interest rate of 6%. The difference in interest rates can result in thousands of dollars in additional interest payments over the life of the loan.

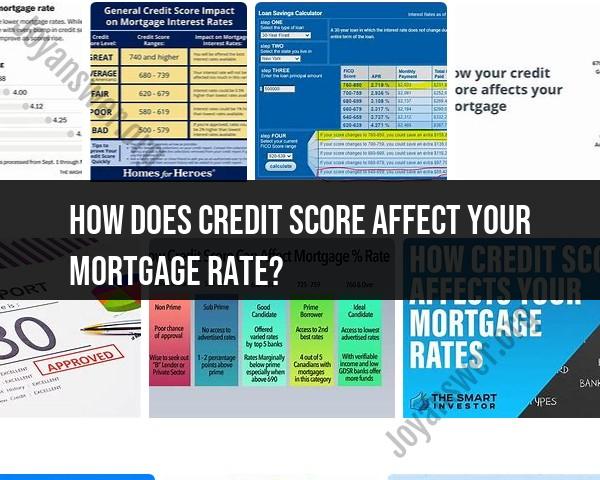

The tiered system of interest rates based on credit score ranges

Lenders typically use a tiered system of interest rates based on credit score ranges. For example, a lender may offer the following interest rates for conventional loans:

- Credit score of 760 or higher: 4.00%

- Credit score of 720-759: 4.25%

- Credit score of 680-719: 4.50%

- Credit score of 640-679: 4.75%

- Credit score of 600-639: 5.00%

As you can see, borrowers with higher credit scores qualify for lower interest rates.

How to estimate the potential mortgage rate with your current credit score

There are a number of online resources that can help you estimate your potential mortgage rate based on your credit score. For example, the Federal Reserve Bank of New York offers a mortgage calculator that allows you to input your credit score, loan amount, and other factors to estimate your monthly mortgage payment.

Improving your credit score to access more favorable mortgage rates

There are a number of things you can do to improve your credit score, including:

- Pay your bills on time and in full each month.

- Keep your credit utilization low.

- Don't open too many new accounts in a short period of time.

- Dispute any errors on your credit report.

If you have a low credit score, you may want to consider working with a credit counselor to develop a plan to improve your score.

Real-world examples of how credit scores influence mortgage affordability

Here are a few real-world examples of how credit scores influence mortgage affordability:

- A borrower with a credit score of 760 and a loan amount of $300,000 may qualify for a mortgage interest rate of 4%. Their monthly mortgage payment would be approximately $1,400.

- A borrower with a credit score of 650 and the same loan amount may only qualify for an interest rate of 6%. Their monthly mortgage payment would be approximately $1,700.

- Over the life of a 30-year mortgage, the borrower with the higher credit score would save over $70,000 in interest payments.

As you can see, your credit score can have a significant impact on your mortgage affordability. By improving your credit score, you can qualify for a lower interest rate and save thousands of dollars over the life of your loan.