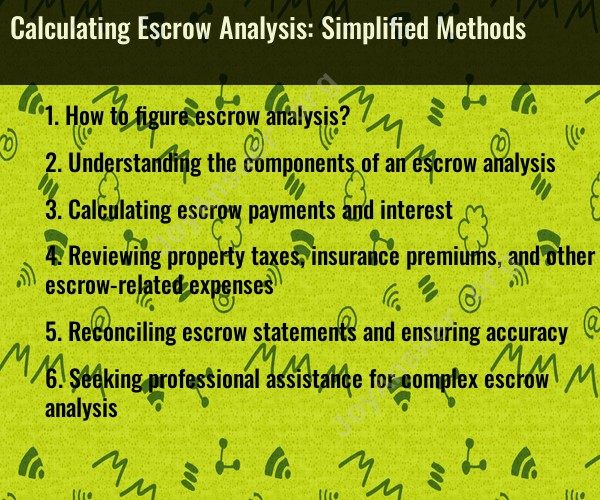

How to figure escrow analysis?

Escrow analysis involves reviewing and adjusting the amount of money held in an escrow account to cover expenses such as property taxes, homeowners insurance, and sometimes mortgage insurance. Here's a simplified overview of how escrow analysis is typically calculated:

Gather Information: Collect all relevant documents, including your mortgage statement, property tax bill, and homeowners insurance policy.

Review Escrow Account Statement: Your mortgage servicer usually provides an annual escrow account statement. Review this statement for the current balances and payments made from the escrow account.

Determine Expenses: Identify the anticipated expenses for the upcoming year. This includes property taxes and insurance premiums. These amounts are usually detailed in the documents you gathered.

Calculate Total Expenses: Add up the anticipated expenses for property taxes, homeowners insurance, and any other expenses paid from the escrow account.

Calculate Adjustments: Compare the total expenses to the current balance in your escrow account. If there's a shortage or surplus, adjustments might be necessary.

Shortage: If the projected expenses exceed the current balance in your escrow account, the shortage might lead to an increase in your monthly escrow payments to cover the shortfall.

Surplus: If there's an excess in the escrow account after covering expenses, you might receive a refund or have lower monthly payments. However, some mortgage servicers might adjust the payments downward, while others might refund the surplus.

Consider Changes: Changes in property taxes or insurance premiums can affect your escrow account. For instance, if property taxes increase, your escrow payments might need adjustment to cover the higher expenses.

Contact Your Servicer: If you have questions or need clarification about the escrow analysis, it's advisable to contact your mortgage servicer. They can explain the calculations and adjustments made to your escrow account.

Remember, the specific calculations and procedures might vary between mortgage servicers, and some lenders might perform escrow analyses more frequently than others. Always refer to your loan documents or contact your mortgage servicer for accurate and personalized information regarding your escrow account.

Understanding the components of an escrow analysis

An escrow analysis is a crucial aspect of mortgage financing, ensuring that homeowners have sufficient funds to cover their property taxes, homeowners insurance, and other escrow-related expenses. By understanding the components of an escrow analysis, homeowners can effectively manage their escrow accounts and avoid potential financial burdens.

Escrow Account Basics: An escrow account is a third-party account held by a mortgage lender to collect and disburse funds for property taxes, homeowners insurance, and other escrow-related expenses. Monthly mortgage payments typically include an escrow component, which is allocated to the escrow account.

Escrow Analysis Statement: An escrow analysis statement is a periodic report provided by the mortgage lender that details the status of the escrow account. It outlines the escrow balance, projected escrow payments, upcoming due dates for property taxes and insurance premiums, and any adjustments or changes to the escrow account.

Key Components of an Escrow Analysis:

a. Escrow Balance: The current amount of funds held in the escrow account.

b. Projected Escrow Payments: The estimated monthly escrow payments for the upcoming year, based on current property tax and insurance premiums.

c. Upcoming Due Dates: The dates when property taxes and insurance premiums are due.

d. Adjustments and Changes: Any adjustments or changes made to the escrow account, such as property tax reassessments or changes in insurance premiums.

Calculating escrow payments and interest

Escrow Payment Formula: The escrow payment formula is used to determine the monthly escrow payment amount. It typically involves the following factors:

a. Annual Escrow Shortage or Surplus: The difference between the projected escrow payments for the year and the actual escrow balance.

b. Number of Monthly Payments: The total number of monthly mortgage payments in a year.

c. Interest Rate: The interest rate applied to the escrow shortage or surplus to account for time value of money.

Interest Calculation: Interest on escrow shortages or surpluses is calculated using the annual interest rate and the remaining balance to be paid.

Reviewing property taxes, insurance premiums, and other escrow-related expenses

Property Taxes: Homeowners should review their property tax assessments to ensure accuracy. Property tax reassessments can impact escrow payments.

Insurance Premiums: Reviewing insurance policies and comparing quotes can help ensure homeowners are getting the best coverage at the best price.

Other Escrow-Related Expenses: Some escrow accounts may include other expenses, such as homeowners association dues or mortgage insurance premiums. Homeowners should be aware of these expenses and factor them into their overall financial planning.

Reconciling escrow statements and ensuring accuracy

Regular Reconciliation: Regularly review escrow statements to ensure accuracy. Compare the statement to property tax bills, insurance premiums, and other escrow-related expenses.

Discrepancies: If discrepancies are found, contact the mortgage lender immediately to resolve any issues. Timely action can prevent overpaying or underpaying escrow.

Seeking professional assistance for complex escrow analysis

For complex escrow situations, such as property tax appeals or insurance disputes, seeking professional assistance from a tax advisor or insurance agent can be beneficial.