What are the basic concepts of microeconomics?

Microeconomics is the branch of economics that focuses on the behavior of individual economic agents, such as households, firms, and consumers, and their interactions in specific markets. Here are some basic concepts of microeconomics:

Scarcity:

- Scarcity is the fundamental economic problem that arises because resources are limited, while human wants and needs are virtually unlimited. Microeconomics examines how individuals and firms make choices to allocate scarce resources efficiently.

Opportunity Cost:

- Opportunity cost is the value of the next best alternative forgone when a decision is made. It represents the trade-off involved in choosing one option over another and is a key concept in microeconomic decision-making.

Supply and Demand:

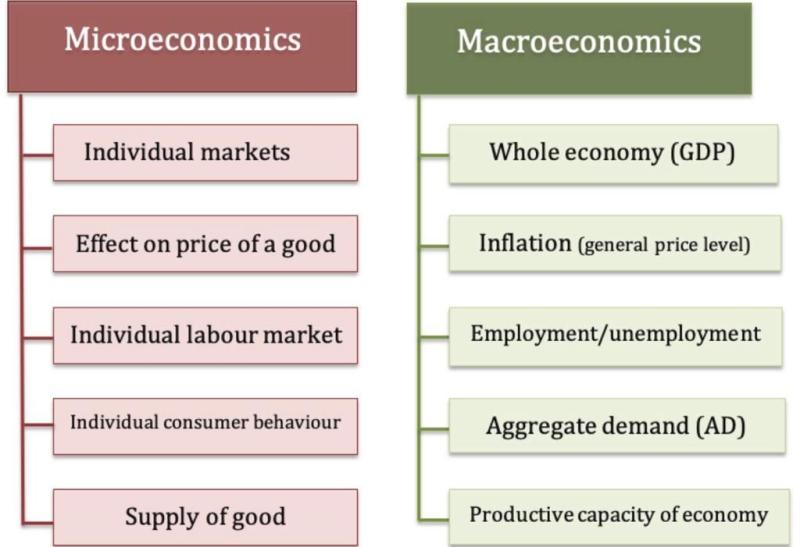

- Supply and demand are foundational concepts in microeconomics. Supply refers to the quantity of a good or service that producers are willing to offer at various prices, while demand represents the quantity that consumers are willing to buy at different prices. The interaction of supply and demand determines market equilibrium, where the quantity supplied equals the quantity demanded.

Elasticity:

- Elasticity measures the responsiveness of quantity demanded or supplied to changes in price. It helps to understand how sensitive consumers and producers are to price changes. Elastic goods or services exhibit significant changes in demand or supply in response to price changes, while inelastic goods or services show less responsiveness.

Consumer Behavior:

- Microeconomics analyzes how consumers make choices regarding the consumption of goods and services. Utility theory examines how individuals maximize their satisfaction or happiness, given their budget constraints and preferences.

Production and Costs:

- Firms make decisions about production levels based on costs and revenue. Concepts such as total cost, average cost, marginal cost, and production functions are crucial for understanding how firms optimize their production processes.

Market Structures:

- Different market structures exist, including perfect competition, monopoly, oligopoly, and monopolistic competition. Microeconomics examines how these market structures influence the behavior of firms, pricing strategies, and overall market outcomes.

Factor Markets:

- Microeconomics considers the markets for factors of production, such as labor, capital, and land. It explores how wages, interest rates, and rents are determined, impacting the income of households and the cost structure of firms.

Game Theory:

- Game theory analyzes strategic interactions between rational decision-makers. It is used to study situations where the outcome for one participant depends on the choices made by others, such as in oligopolistic markets.

Externalities:

- Externalities are spillover effects of economic activities that affect third parties who are not directly involved in the transaction. Microeconomics examines how externalities can lead to market failures and explores policy options to address them.

These basic concepts provide a foundation for understanding the behavior of individual economic agents and the functioning of markets in microeconomics. They are essential for analyzing economic decision-making, resource allocation, and the efficiency of market outcomes at the microeconomic level.

What foundational ideas form the basis of microeconomics?

Microeconomics delves into the intricate world of individual decision-making and interactions within specific markets. Several foundational ideas underpin this fascinating field, guiding analysis and helping us understand how resources are allocated and prices are determined. Here are some of the key principles that form the base of microeconomics:

1. Scarcity and Choice: This fundamental truth acknowledges that resources are limited. Individuals, households, and firms constantly face choices about how to allocate these resources to fulfill their needs and wants. This inherent trade-off between various options shapes much of microeconomic analysis.

2. Incentives and Optimization: People respond to incentives, motivated to maximize their own benefit (utility) given their resources and constraints. Understanding how incentives influence behavior is crucial for predicting individual choices, such as consumer spending patterns, firm production decisions, and labor market participation.

3. Supply and Demand: This powerful framework explores the interaction between buyers and sellers in a market, explaining how price is determined by the quantities of a good or service that buyers are willing and able to purchase (demand) and that sellers are willing and able to supply. Analyzing shifts in supply and demand curves helps us understand price changes, market equilibrium, and resource allocation.

4. Market Structure: Different market structures, such as perfect competition, monopoly, oligopoly, and monopolistic competition, impact competition, pricing behavior, and consumer welfare. Microeconomic analysis explores how market structure influences the efficiency of resource allocation and the distribution of gains among buyers and sellers.

5. Marginal Analysis: This analytical tool involves examining the change in a variable, such as cost or benefit, as another variable changes slightly. Microeconomists use marginal analysis to understand decision-making at the margin, such as price setting by firms or consumption choices by individuals.

6. Efficiency and Trade: Specialization and trade allow individuals and firms to focus on their comparative advantages and exchange goods and services at mutually beneficial terms. Microeconomics explores how trade can increase overall efficiency and welfare within an economy and even across national borders.

7. Information and Uncertainty: Not all information is perfect, and decisions are often made with incomplete knowledge. Microeconomics examines how information asymmetry (unequal access to information) and uncertainty can affect market outcomes and individual behavior.

These are just some of the foundational ideas that form the basis of microeconomics. As you delve deeper into the field, you'll encounter various models and theories that utilize these principles in different ways to analyze specific economic phenomena, such as consumer behavior, firm pricing strategies, market competition, and resource allocation.

Remember, microeconomics is a dynamic and multifaceted field, and these foundational ideas serve as a springboard for continuous exploration and discovery. Feel free to ask further questions about specific microeconomic concepts or delve deeper into any of the principles mentioned above!