What are the basics of Economics?

Economics is a social science that studies the production, distribution, and consumption of goods and services. It involves analyzing how individuals, businesses, and governments make choices to allocate resources to satisfy their wants and needs. Here are some foundational concepts and basics of economics:

Scarcity:

- Scarcity is a fundamental economic problem that arises because resources are limited, while human wants and needs are virtually unlimited. This forces individuals and societies to make choices about how to allocate their scarce resources.

Supply and Demand:

- Supply and demand are the forces that determine prices and quantities in a market. The law of demand states that as the price of a good or service decreases, the quantity demanded increases, and vice versa. The law of supply states that as the price of a good or service increases, the quantity supplied increases, and vice versa.

Opportunity Cost:

- Opportunity cost is the value of the next best alternative that must be forgone when a choice is made. It reflects the idea that resources used for one purpose cannot be used for another.

Marginal Analysis:

- Economists often analyze decisions at the margin, considering the additional or marginal benefit of an action compared to its additional or marginal cost. Rational decision-making involves pursuing an action as long as the marginal benefit exceeds the marginal cost.

Factors of Production:

- The factors of production are the resources used in the production of goods and services. They include:

- Land: Natural resources like water, minerals, and agricultural land.

- Labor: Human effort, skills, and time.

- Capital: Physical capital (machinery, tools) and human capital (knowledge, skills).

- Entrepreneurship: The ability to innovate, take risks, and organize resources.

- The factors of production are the resources used in the production of goods and services. They include:

Economic Systems:

- Economic systems define how a society organizes and allocates its resources. Common types include:

- Market Economy: Decisions are made by individuals and businesses based on supply and demand.

- Command (Planned) Economy: Decisions are made by a central authority, often the government.

- Mixed Economy: Combines elements of both market and command economies.

- Economic systems define how a society organizes and allocates its resources. Common types include:

Inflation and Deflation:

- Inflation is the increase in the general price level of goods and services over time. Deflation is the opposite, involving a decrease in prices. Both can have significant effects on an economy.

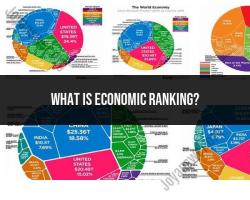

Gross Domestic Product (GDP):

- GDP measures the total value of goods and services produced within a country's borders over a specific period. It is a key indicator of a nation's economic health.

Trade:

- International trade allows countries to specialize in the production of goods and services in which they have a comparative advantage. This promotes efficiency and can lead to increased overall prosperity.

Economic Indicators:

- Various economic indicators, such as unemployment rates, interest rates, and consumer confidence, provide insights into the health and performance of an economy.

These concepts provide a foundational understanding of the principles that govern economic decision-making at individual, business, and societal levels. Economics is a broad field with various branches, including microeconomics, macroeconomics, and international economics, each delving into specific aspects of economic behavior and systems.

What fundamental principles form the basis of Economics as a discipline?

Several fundamental principles form the basis of Economics as a discipline. These principles provide a framework for understanding how individuals, firms, and societies make choices under conditions of scarcity. Here are some of the most important:

1. Scarcity and Choice:

- Resources are limited, while human wants are unlimited. This fundamental dilemma of scarcity forces individuals and societies to make choices about how to allocate resources to satisfy their wants. These choices involve trade-offs, as one choice requires forgoing another.

2. Rational Choice and Utility:

- Individuals are assumed to act rationally, seeking to maximize their own utility (satisfaction or well-being) with the resources available. This principle helps explain how individuals make decisions about consumption, production, and investment.

3. Supply and Demand:

- The interaction between supply (the amount of a good or service producers are willing and able to sell at different prices) and demand (the amount of a good or service consumers are willing and able to buy at different prices) determines the market price. This principle explains how prices are determined and how they allocate resources in markets.

4. Marginal Utility:

- The additional utility (satisfaction) gained from consuming one more unit of a good or service. This principle suggests that as individuals consume more of a good, the additional satisfaction they get from each additional unit decreases. This influences consumption patterns and pricing strategies.

5. Incentives and Opportunity Cost:

- Individuals respond to incentives, such as prices, taxes, and subsidies, which influence their choices. The opportunity cost of a choice is the benefit forgone by choosing one option over another. Understanding opportunity costs helps individuals and policymakers make efficient decisions.

6. Efficiency and Trade:

- Efficiency refers to a state where resources are allocated to their most productive uses. Trade allows individuals and societies to specialize in production and exchange goods and services, potentially leading to increased efficiency and overall well-being.

7. Institutions and Property Rights:

- Institutions, such as legal systems and markets, define the rules of the game in an economy. Property rights define ownership of resources and influence how resources are used. Strong institutions and well-defined property rights are essential for efficient economic functioning.

These are just some of the fundamental principles that shape the study of Economics. Understanding these principles can provide valuable insights into how individuals, firms, and societies make choices, allocate resources, and interact in the marketplace.

It's important to remember that these principles are simplifications of complex realities and may not always perfectly explain economic phenomena. However, they provide a useful starting point for understanding the key drivers of economic behavior and outcomes.

I hope this explanation is helpful! Feel free to ask any further questions you may have about these principles or other aspects of Economics.