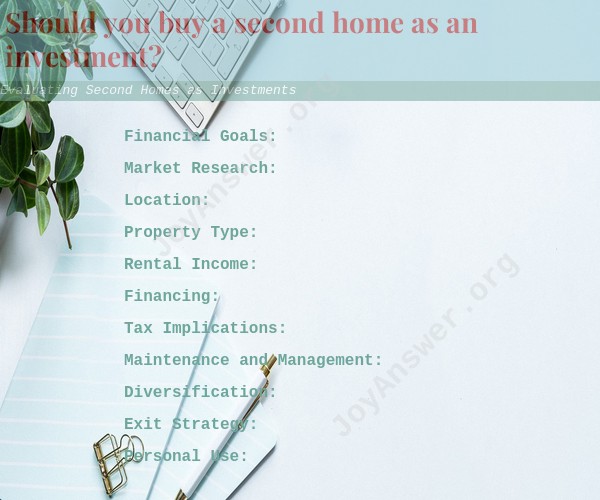

Should you buy a second home as an investment?

Whether you should buy a second home as an investment depends on various factors, including your financial goals, risk tolerance, and personal circumstances. Here are some key considerations to help you evaluate whether a second home makes sense as an investment:

Financial Goals: Clarify your financial objectives. Are you looking for a source of rental income, long-term capital appreciation, or a combination of both? Your goals will influence the type of property and location you choose.

Market Research: Research the real estate market in the area where you plan to buy. Consider factors such as property appreciation rates, rental demand, and potential for growth. A strong and stable market is more likely to yield good returns.

Location: Location is crucial in real estate. Choose a location that has the potential for growth and offers amenities that appeal to renters or future buyers.

Property Type: Decide whether you want to invest in a vacation home, a rental property, or a fix-and-flip opportunity. Each type has its own set of considerations and potential returns.

Rental Income: If you plan to rent out the property, analyze the rental market in the area. Calculate expected rental income and expenses, including property management fees, maintenance costs, and property taxes.

Financing: Consider how you'll finance the second home. Mortgage interest rates, down payments, and the impact on your overall financial situation are important factors to weigh.

Tax Implications: Understand the tax implications of owning a second home. Tax laws can vary by location and change over time. Consult with a tax advisor to assess the potential tax benefits or liabilities.

Maintenance and Management: Owning a second home requires ongoing maintenance and management. You may need to budget for repairs, property management fees, and other costs.

Diversification: Consider how a second home fits into your overall investment portfolio. Diversifying across different asset classes, such as stocks, bonds, and real estate, can help manage risk.

Exit Strategy: Have a clear exit strategy in mind. Know when and under what circumstances you might sell the property, and be prepared for market fluctuations.

Personal Use: If you plan to use the second home for personal enjoyment, factor in the costs associated with your own use, such as travel expenses and time away from work.

Long-Term vs. Short-Term: Determine whether you're looking for a short-term investment with the potential for quick returns or a long-term asset that may appreciate over time.

It's important to conduct thorough research and, if needed, consult with financial advisors or real estate professionals before making a decision. While a second home can be a rewarding investment, it also comes with risks and responsibilities. Careful consideration of your goals and circumstances is key to making an informed choice.