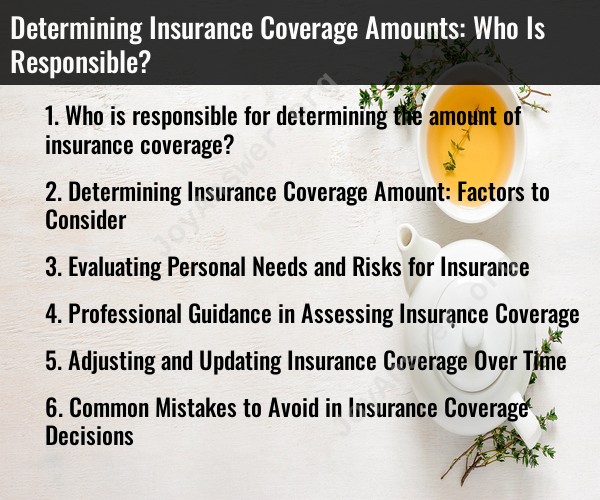

Who is responsible for determining the amount of insurance coverage?

The responsibility for determining the amount of insurance coverage primarily falls on the policyholder or the insured individual. When purchasing insurance, whether it's for health, auto, home, life, or any other type of coverage, the policyholder must make decisions regarding the level of coverage and the corresponding coverage limits. Here's how it works for various types of insurance:

Health Insurance: Individuals or employers (in the case of group health insurance) are responsible for selecting health insurance plans and coverage levels. They choose the type of plan, deductible, co-pays, and other features that suit their needs.

Auto Insurance: Vehicle owners are responsible for determining the amount of auto insurance coverage. They choose the types of coverage, such as liability, comprehensive, collision, and the coverage limits for each.

Home Insurance: Homeowners decide on the amount of coverage for their property, personal belongings, and liability when purchasing homeowners' insurance. They also choose the deductible and policy endorsements.

Life Insurance: Individuals or policyholders select the amount of life insurance coverage based on factors such as their financial obligations, income replacement needs, and future expenses, including funeral costs.

Business Insurance: Business owners are responsible for determining the level of insurance coverage for their company. This includes coverage for property, liability, workers' compensation, and more.

Liability Insurance: Those seeking liability insurance, whether it's general liability for businesses or personal liability, need to decide on coverage limits that protect their assets.

Professional Liability Insurance: Professionals like doctors, lawyers, and architects are responsible for choosing the amount of professional liability insurance coverage they need to protect against malpractice claims.

Umbrella Insurance: Individuals and businesses can purchase umbrella insurance to provide additional liability coverage above and beyond their primary policies. They decide on the coverage limits for this extra protection.

The insurance company plays a role in the process by offering different policy options and coverage limits, but the final decisions are made by the insured party. It's essential for individuals and businesses to carefully assess their needs, risks, and financial situations when determining the appropriate amount of insurance coverage. Additionally, it's advisable to periodically review and adjust coverage amounts to reflect changes in circumstances and needs. Insurance agents and brokers can provide guidance and information to help individuals and businesses make informed decisions about their coverage.

Determining Insurance Coverage Amount: Factors to Consider

When determining how much insurance coverage you need, there are a number of factors to consider, including:

- Your assets: How much would it cost to replace your home, belongings, and other assets if they were destroyed or lost?

- Your income: How much would you need to maintain your lifestyle if you were unable to work due to illness or injury?

- Your dependents: Do you have children or other dependents who would rely on your income if you were unable to work?

- Your debts: How much debt would you leave behind if you died?

- Your lifestyle: What kinds of activities do you enjoy and what are your financial goals?

Evaluating Personal Needs and Risks for Insurance

Once you have considered all of the relevant factors, you can begin to evaluate your personal needs and risks for insurance. This involves identifying the areas where you are most vulnerable financially and making sure that you have adequate coverage in place.

For example, if you have a young family and a large mortgage, you may want to purchase more life insurance than someone who is single and has no dependents. Similarly, if you own a business, you may need to purchase commercial liability insurance to protect yourself from lawsuits.

Professional Guidance in Assessing Insurance Coverage

If you are unsure about how much insurance coverage you need or what types of insurance are right for you, it can be helpful to consult with a professional insurance agent or broker. They can help you assess your needs and risks and develop an insurance plan that is tailored to your individual circumstances.

Adjusting and Updating Insurance Coverage Over Time

Your insurance needs will change over time as your life circumstances change. For example, if you get married, have children, or buy a new home, you may need to adjust your coverage accordingly. It is also important to review your insurance coverage regularly to make sure that it is still adequate and that you are not overpaying for coverage that you do not need.

Common Mistakes to Avoid in Insurance Coverage Decisions

Here are some common mistakes to avoid when making insurance coverage decisions:

- Underinsuring: Not having enough insurance coverage can leave you financially vulnerable in the event of a loss.

- Overinsuring: Buying too much insurance coverage can waste your money.

- Not understanding your policy: Make sure you understand the terms and conditions of your insurance policy before you sign it.

- Failing to review your coverage regularly: Your insurance needs will change over time, so it is important to review your coverage regularly to make sure that it is still adequate.

Conclusion

Making informed decisions about insurance coverage is important for protecting your financial well-being. By considering your personal needs and risks, seeking professional guidance, and adjusting your coverage over time, you can ensure that you have the coverage you need to protect yourself and your loved ones.