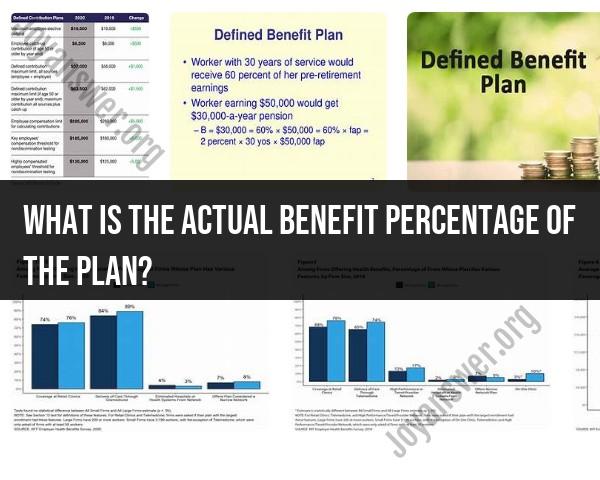

What is the actual benefit percentage of the plan?

The "actual benefit percentage" is a term often used in the context of retirement plans, particularly in the United States. It refers to the percentage of your final average salary that you can expect to receive as a retirement benefit from a defined benefit pension plan. Defined benefit plans are employer-sponsored retirement plans that promise a specific monthly benefit to employees upon retirement, based on a formula that typically considers factors such as years of service and final average salary.

The actual benefit percentage is determined by the plan's formula and is a key factor in calculating your retirement income. It can vary widely depending on the specific plan and the terms set by your employer or the pension plan provider. The formula for calculating the monthly retirement benefit may look something like this:

Monthly Benefit = Actual Benefit Percentage × Final Average Salary

In this formula:

- "Monthly Benefit" is the amount you'll receive as your monthly retirement income.

- "Actual Benefit Percentage" is the percentage of your final average salary determined by the plan's formula.

- "Final Average Salary" is typically the average of your highest earning years, often the last three to five years of your career.

The actual benefit percentage can vary based on factors such as your years of service, age at retirement, and the specific formula used by the pension plan. Some plans may offer a higher actual benefit percentage for longer service or for employees who retire at a later age.

It's essential to review your plan's documents or consult with your employer's benefits department to understand the specific details of the plan, including how the actual benefit percentage is determined and what factors may affect it. Additionally, keep in mind that defined benefit pension plans are becoming less common, with many employers shifting to defined contribution plans like 401(k)s, where the retirement benefit depends on contributions and investment performance rather than a fixed formula.

How is the actual benefit percentage of a plan determined or calculated?

The actual benefit percentage of an insurance or benefit plan is the percentage of the total cost of covered services that the plan will pay. It is calculated by dividing the total amount of benefits paid by the total amount of covered services.

For example, if an insurance plan pays out $100,000 in benefits for covered services that total $200,000, the actual benefit percentage would be 50%.

What factors and considerations impact the actual benefit percentage of an insurance plan?

A number of factors can impact the actual benefit percentage of an insurance plan, including:

- The type of plan: Some types of plans, such as HMOs and PPOs, typically have higher benefit percentages than other types of plans, such as indemnity plans.

- The deductible and coinsurance: The deductible is the amount of money that a policyholder must pay out-of-pocket before the insurance plan begins to pay benefits. The coinsurance is the percentage of the cost of covered services that the policyholder must pay after meeting the deductible. Higher deductibles and coinsurances will result in lower benefit percentages.

- The network of providers: If an insurance plan has a large network of providers, it is more likely that policyholders will be able to find in-network providers who accept the plan's benefits. This can lead to higher benefit percentages, as policyholders will not have to pay as much out-of-pocket for covered services.

- The policyholder's health: Policyholders with chronic health conditions may have lower benefit percentages, as they are more likely to use more medical services.

How to assess the real value and advantages offered by a specific insurance or benefit plan?

When assessing the real value and advantages offered by a specific insurance or benefit plan, it is important to consider the following factors:

- The type of plan: Consider the type of plan and whether it is a good fit for your needs. For example, if you have a chronic health condition, you may want to consider a plan with a lower deductible and coinsurance.

- The network of providers: Make sure that the plan has a network of providers that is convenient for you and that includes your preferred doctors and hospitals.

- The cost of the plan: Compare the cost of the plan to other available plans and to your budget.

- The benefits offered: Consider the benefits that are important to you and make sure that the plan offers those benefits.

It is also important to read the plan's fine print carefully before enrolling. This will help you to understand the plan's coverage and limitations.

Here are some additional tips for assessing the real value and advantages offered by a specific insurance or benefit plan:

- Compare the plan to other available plans. This will help you to determine whether the plan is competitively priced and offers the benefits that are important to you.

- Talk to your doctor or other healthcare provider. They can help you to understand the plan's coverage and how it would apply to your specific needs.

- Contact the insurance company directly. They can answer your questions about the plan and help you to enroll.

By following these tips, you can assess the real value and advantages offered by a specific insurance or benefit plan and choose the plan that is best for you.